How Much Are My Savings Bonds Worth?

From being safe to having no income tax charged on them, U.S savings bonds are a great form of investment. We’ll be sharing how you can cash your savings bonds.

In today’s ever-changing financial landscape, individuals seeking stable and secure investment options often turn to savings bonds. Government-issued savings bonds have long been regarded as reliable for building long-term wealth. These bonds offer a haven for investors by providing guaranteed returns, making them an attractive choice amidst economic uncertainties.

All this depends on the type of savings bonds and the current interest at the time of purchase. It takes several years for savings bonds to mature; hence it’s a great investment if you’re willing to wait out those years.

Savings bonds are a type of federal government debt. When you purchase a savings bond, you’re technically lending money to the government and agreeing to allow the government to repay that amount at a specific interest rate.

While saving bonds are a form of long-term investment, there eventually comes a time when you will want to redeem them. Perhaps you’re redeeming them because you’re returning to school, have decided to retire, or for several other reasons; it’s your right to know how much your savings bond is worth.

This article delves into savings bonds, examining their value and potential returns. We explore the savings bonds available, including Series EE, Series I, etc., while highlighting their benefits and how you can redeem them. Read on below to understand.

U.S. Savings Bonds

There are several features in the U.S. savings bond. Most people find these bonds attractive as they’re not subjected to either state or local income taxes. However, these bonds can’t be transferred easily and are non-negotiable.

Here are some features:

- Non-Marketable: S. savings bonds are designed to be non-marketable, which means an investor can only purchase them from the U.S. government and can’t be sold to another investor.

Hence, when an investor redeems his savings bond, he will receive his original investment. Moreover, since the savings bond is registered with the government, any damaged or lost savings bond certificate can be replaced or reissued. - Purchase: The U.S. savings bonds can only be purchased and further redeemed electronically via the TreasuryDirect website, which the government administers.

The investor needs to open an account on their website and provide their Social Security Number, savings or checking account, and email address. - Interest payment: S. savings bonds are zero-coupon bonds that require no interest until they’re eventually redeemed, or once they reach the maturity date. Any interest paid at maturity or redemption is electronically issued to the investor’s designated bank account.

- Early redemption: The number of years it takes for a savings bond to mature differs, but it is usually between 15 and 30 years. The bondholder has to wait at least 12 months after the initial investment before deciding to redeem their savings bond and will receive the face value and interest.Deciding to redeem a savings bond after five years will incur the investor zero penalty.

- Tax consequences: Interests earned from savings bonds have no state or local taxes charged. However, you’ll still be charged federal taxes only during the year the bond matures or is redeemed.

Types of U.S. Savings Bonds

Various types of U.S. savings bonds have been distributed over the years, the government no longer offers some of these, but investors still own them. Depending on every individual bondholder’s situation, you may own a savings bond that is no longer earning interest or can’t be purchased any longer but is still redeemable for cash value.

Currently, two types of savings bonds are issued by the U.S. Treasury – Series EE and Series I savings bonds. Series E and Series HH savings bonds might still be held by savers in the U.S.

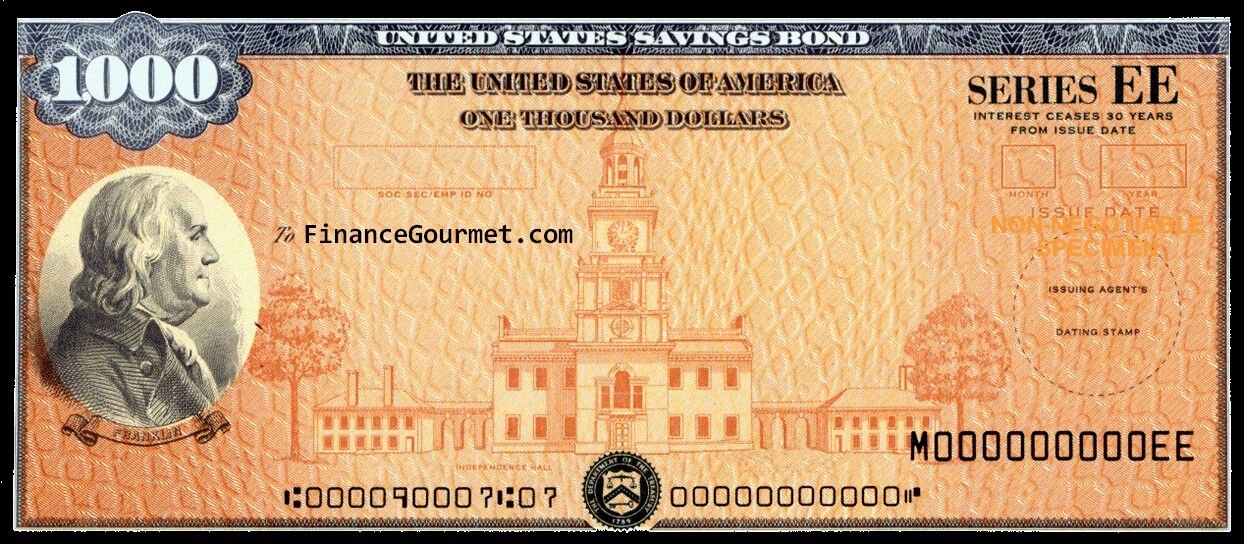

Series EE

Savings Bonds Series EE can be purchased electronically through TreasuryDirect, and you get to earn a fixed interest rate. Series EE bonds bought between Nov. 1, 2018, to April 30, 2019, are 0.10% of interest and are sold at face value.

Series EE bonds earn interest until you redeem the bond for 20 years. Moreover, you can only redeem the bond after one year of having purchased them, and if you redeem it before the five years mark, you need to forfeit the previous three months with interest.

Series I

Similarly to Series EE bonds, Series I Savings Bonds can be purchased electronically via TreasuryDirect and on paper using your IRS tax refund. There are two types of interest on Series I bonds; a fixed interest rate available at the time of purchase and an inflation rate calculated twice yearly.

Series I bonds are sold at full value and reach maturity after 30 years. The redemption rules for Series I bonds are identical to those for Series EE bonds. The composite rate assigned to Series I bonds issued between November 1, 2019, and April 30, 2020, is 2.22%. This rate is applicable during the initial six months of bond ownership.

Series E

In addition to the above savings bonds, some older bonds are no longer being sold, but you might still be paying interest. If you own these savings bonds, you may prefer to redeem them sooner.

One of them is the Series E Savings Bonds that was introduced in 1941. These bonds were typically purchased to help fund the war efforts. However, they were eventually replaced by Series EE bonds in 1980.

The last Series E bonds stopped paying interest in 2010, so it’s best to redeem this bond if you still own them.

Series HH

Series HH Savings Bonds were distributed from 1980 to 2004, with a maturity period of 20 years, so technically, some of these bonds are still earning interest until 2024. To redeem the Series HH bonds, you’ll need it to Treasury Retail Securities Services at a specific address with a signed form.

Your bank is not eligible to cash these bonds for you but can assist you with the process.

How Much Are Your Savings Bonds Worth?

Discovering the value of your savings bonds involves considering various factors, including bond type, issuance date, and purchase price. If you hold Series EE or Series I bonds, accessing your TreasuryDirect online account will unveil the current value.

For owners of older paper bonds, discontinued since 2012 but still redeemable, a handy free calculator tool on TreasuryDirect can reveal the current worth. Simply input your bond’s details: denomination, serial number, and issuance date. These bonds never expire but cease accruing interest upon maturity. The calculator can also forecast future values, aiding in strategic planning for bond redemption.

Accompanying the calculator are detailed instructions on managing bond inventory, understanding future values, and calculating interest for IRS reporting upon maturity.

For electronic bonds, accessing your TreasuryDirect account offers a convenient solution. Log in and navigate to the current holding tab to find the bond’s current value.

Knowing your bond’s value empowers decisions on whether to redeem it for cash or allow it to mature fully. Remember, letting a bond mature before redemption often yields optimal returns.

By utilizing these tools and resources, you can easily stay informed about your savings bond portfolio, ensuring sound financial planning and decision-making.

Tax Implications on Redeeming Your Savings Bonds

As mentioned earlier, your U.S. savings bonds are only subjected to federal income tax, not state or local income taxes. Your savings bond interest can be further subjected to a federal or state inheritance tax, excise tax, and federal gift, depending on your current tax situation.

The interest income from your savings bonds can be reported to the IRS whenever the interest is accrued, or you can also report the interest income at the point of redemption. It’s best to speak to a professional tax advisor to know which reporting method would best suit your overall tax situation.

Hence, before you decide to redeem your savings bonds, be sure to understand every tiny detail of your savings bonds and be mentally prepared to deal with possible tax implications or interest penalties.

Also, be prepared to talk to a professional financial advisor about utilizing your savings to support your long-term financial goals.

How to Redeem Savings Bonds?

There is more than one way to redeem your savings bonds in cash. You can easily redeem your savings bonds through your online TreasuryDirect account if you purchased them electronically. The redeemed cash will be deposited into your savings or checking account within the next few business days.

However, if your bond was purchased on paper, you must head to your local bank or a credit union to redeem it. According to the Treasury Department, more than 95% of savings bonds are often cashed at local banks and credit unions.

Be mindful that some other older savings bonds can’t be redeemed at your local bank or credit union. Hence you’ll then need to fill out a special FS Form 1522 and mail the bond to the Treasury Department’s Treasury Retail Security Services with clear deposit instructions and a certified signature on it.

For example, if your bank or credit union is not able to cash an older savings bond of yours, or if you have inherited an old savings bond, the bank will still be able to help talk you through the entire redeeming process. It can further certify the signature on the Treasury Form.

It’s important to note that cashing in the bond before it matures in 20 years may not yield the level of returns, and you could lose the last three months of interest if redeemed before the fifth year.

Financial advisers recommend against purchasing savings bonds unless they have a specific purpose in your portfolio. However, if you choose to hold onto the bond, it will continue to earn interest for up to 30 years, making it even more valuable over time.

FAQs

Where can you purchase savings bonds from?

Savings bonds can be bought through the U.S. Treasury via TreasuryDirect.gov. An exception is that you can get a paper Series I bond, up to $5,000, by filing IRS Form 8888 with your tax return.

Who is eligible to buy savings bonds?

Anyone 18 or older with a Social Security number and who is a U.S. citizen, U.S. resident, or U.S. government employee can buy U.S. savings bonds. They can also be given as gifts, provided the recipient has a TreasuryDirect account and a Social Security number.

What are the purchase limits for savings bonds?

You can buy either bond in any amount, up to $10.000 per year. With a tax refund of at least $5,000, you can get a Series I paper bond, raising the yearly maximum to $25,000.

How can savings bonds be cashed in?

Once the electronic bonds are at least a year old, they can be cashed in through your TreasuryDirect account. Paper bonds can be chased in at any bank branch, while Series HH paper bonds need to be mailed to the U.S. Treasury and will accrue interest until 2024.

Are savings bonds a good investment?

Deciding if savings bonds are a good investment depends on factors like your ability to hold them long-term, potential returns compared to other investments, and willingness to take on risk. Savings bonds have low risk since they are backed by the U.S. government’s “full faith and credit.”

Conclusion

When your bonds reach maturity and cease earning interest, don’t delay in cashing them—take prompt action to maximize your returns.

Investing in savings bonds offers unparalleled simplicity and minimal paperwork, making them an attractive option for many. Once purchased, bonds require no ongoing management until you opt to redeem them.

Regardless of your motivation for redeeming savings bonds, it’s crucial to assess their current value. Ensure that cashing them aligns with significant financial objectives, actively contributing to your overall financial strategy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}