How To Calculate Debt To Equity Ratio?

Investors often take into account the company’s debt-to-equity ratio when assessing the stock. If the number is roughly 3, it means that for every shareholder dollar, there is $3 of debt. What’s high or low, or good or bad, depends on the sector. Financial industry companies tend to have the highest numbers, say, 20, while stable manufacturing companies ha a low number. Having a number lower than 1, say, 0.45, could invite a buyout. Knowing what the ratio is and what is a good debt to equity ratio can help you make effective investment decisions.

The article explores how to calculate the debt to equity ratio, D/E ratio formula, its interpretation, and long-term debt to equity ratio in depth.

What Is Debt To Equity Ratio?

Debt to equity ratio (also termed as a debt-equity ratio) is a long-term solvency ratio that shows the soundness of the long-term financial policies of a company. It shows the connection between the portion of assets financed by creditors and the portion of assets financed by stockholders. As the debt to equity ratio portrays the relationship between external equity (liabilities) and internal equity (stockholder’s equity), it is also known as the “external-internal equity ratio”.

The debt and equity components are taken from the right side of the firm’s balance sheet. Debt is what the firm owes its creditors plus interest. In the debt to equity ratio, only long-term debt is incorporated into the equation. Long-term debt is debt that has a maturity of more than one year. Long-term debt consists of mortgages, long-term leases, and other long-term loans.

If you have a $50,000 loan and $20,000 is due this year, the $20,000 is considered a current liability and the remaining $30,000 is considered a long-term liability or long-term debt. When calculating the debt to equity ratio, you take the entire $30,000 in the numerator in the debt to equity ratio formula.

Shareholder’s equity, if your firm is incorporated, is the sum of paid-in capital, the contributed capital above the par value of the stock, and retained earnings. The company’s retained earnings are the profits not paid out as dividends to shareholders. Contributed capital is the value shareholders paid in for their shares.

Shareholder’s equity is the value of the company’s total assets less its total liabilities. The remainder is the shareholder ownership of the company. It is the denominator in the debt to equity formula.

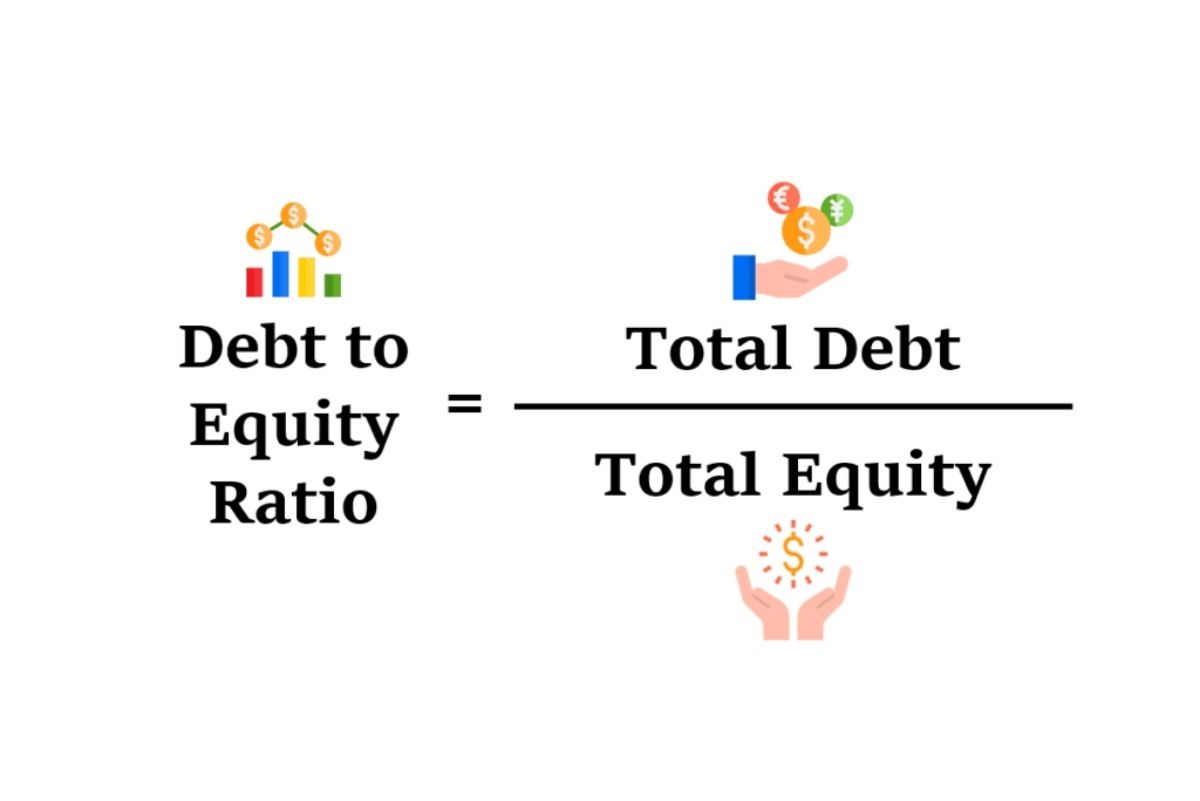

Debt to Equity Ratio Formula

The formula for the debt to equity ratio is given below:

Debt/Equity =

The information required for the D/E ratio is on a company’s balance sheet. The balance sheet requires total shareholder equity to equal assets minus liabilities, which is a rearranged version of the balance sheet equation:

Assets = Liabilities + Shareholder Equity

These balance sheet categories may have individual accounts that would not normally be referred to as “debt” or “equity” in the conventional sense of a loan or the book value of an asset. Because the ratio can be affected by retained earnings/losses, intangible assets, and pension plan adjustments, further research is mostly needed to understand a company’s true leverage.

Debt To Equity Ratio Example

Below are some debt to equity ratio examples to make it easier for you to understand how to calculate debt to equity ratio.

Example 1: XYZ company has applied for a loan. The lender of the loan requests you to calculate the debt to equity ratio as a part of the long-term solvency test of the company.

The “Liabilities and Stockholders’ Equity” section of the balance sheet of XYZ company is given below:

Required: Calculate debt to equity ratio of XYZ company.

Solution:

Debt to equity ratio = Total liabilities/Stockholders’ equity

= 7,250/8,500

= 0.85

The debt to equity ratio of XYZ company is 0.85 or 0.85: 1. This implies that the liabilities are 85% of stockholders’ equity or we can also say that the creditors provide 85 cents for each dollar provided by stockholders to finance the assets.

If the debt to equity ratio and one of the other two-equation elements are given, we can work out the third element. Consider the example 2 and 3.

Example 2 – calculation of stockholders’ equity when total liabilities and debt to equity ratio are given.

The PTC company has total liabilities of $937,500 and a debt to equity ratio of 1.25. Calculate total stockholders’ equity of Petersen Trading Company.

Solution:

Debt to equity ratio = Total liabilities/Total stockholder’s equity

or

Total stockholder’s equity = Total liabilities/Debt to equity ratio

= $937,500/1.25

= $750,000

Example 3 – calculation of total liabilities when stockholders’ equity and debt to equity ratio are given.

The Simon Corporation’s debt to equity ratio for the last year was 0.75 and stockholders’ equity was $750,000. What were the total liabilities of the corporation?

Solution

Debt to equity ratio = Total liabilities/Total stockholder’s equity

or

Total liabilities = Stockholders’ equity/Debt to equity ratio

= $750,000/0.75

= $1000,000

Debt-To-Equity Ratio High Or Low

Each industry has a distinct debt to equity ratio standards, as some industries have a tendency to use more debt financing than others. A debt ratio of 0.5 means that there are half as many liabilities than there is equity. In other words, the assets of the company are financed 2-to-1 by investors to creditors. This entails that investors own 66.6 cents of every dollar of company assets while creditors only own 33.3 cents on the dollar. Debt to equity ratio of 1 would suggest that investors and creditors have an equal share in the business assets.

A lower debt to equity ratio usually indicates a more financially stable business. Companies with a higher debt to equity ratio are deemed as riskier to creditors and investors than companies with a lower ratio. Unlike equity financing, debt must be repaid to the lender. Since debt financing also needs debt servicing or regular interest payments, debt can be a far more costly form of financing than equity financing. Companies leveraging large amounts of debt might not be able to make the payments.

Creditors see a higher debt to equity ratio as risky because it indicates that the investors haven’t funded the operations as much as creditors have. In other words, investors don’t have as much stake in the game as the creditors do. This could portray that investors are reluctant to fund business operations because the company isn’t doing well. Lack of performance might also be the reason why the company is looking for extra debt financing.

What Is A Good Debt To Equity Ratio

A good debt-to-equity ratio will be likely to vary widely by industry, but the general agreement is that it should not be above a level of 2.0. While some very large companies in fixed asset-heavy industries (such as mining or manufacturing) may have ratios higher than 2, these are the exception rather than the rule.

A D/E ratio of 2 signifies that the company derives two-thirds of its capital financing from debt and one-third from shareholder equity, so it borrows twice as much funding as it owns (2 debt units for every 1 equity unit). A company’s management will, therefore, try to target a debt load that is in accordance with a favorable D/E ratio in order to function without fretting about defaulting on its bonds or loans.

Long-Term Debt To Equity Ratio

Long term debt to equity ratio is a leverage ratio that compares the total amount of long-term debt against the shareholders’ equity of a company. The objective of this ratio is to figure out how much leverage the company is taking. A higher ratio means the company is taking on more debt. This, in turn, often makes them more susceptible to financial risk.

Long term debt to equity is a modification of the debt to equity ratio. Debt to equity takes into account short-term debt, long-term debt, and other fixed payments. However long-term debt to equity only calculates long-term debt. Some analysts have a preference for the latter ratio since long-term debt is likely to increase the burden and has relatively higher risks to other liabilities.

Furthermore, apart from the current ratio, looking at one company’s past results is also a great idea. That way, we can examine whether the level of leverage is increasing or decreasing. Even if a company has a high long term debt to equity ratio, it would still have a better standing if the ratio lowers year-over-year.

Long Term Debt to Equity Ratio Formula

LTD/E =

To compute the value of long-term debt, you should be able to find it recorded in the liabilities section of the company’s balance sheet. Long-term debt contains loans or other debt obligations that are due in more than 12 months. Any kind of debts required to be paid off in less than one year, i.e. short-term debt, is excluded in the calculation.

Remember that debt is different from liability. Liabilities include all types of debt, but not all liabilities are debts. Debts fund an entity—be it an individual or a corporation—borrowed that needs to be paid back before it’s due. Furthermore, liabilities are something, e.g. money, goods, service, an entity owes to another party but not always in the form of debt. Some of the examples of non-debt liabilities are wages and deferred revenue (income received by a

company for not yet delivered service to customers).

To calculate the long-term debt to equity ratio you need to simply see the long-term debt value under non-current or long-term liabilities. However, keep in mind that we are not adding all of the long-term liabilities (as some of them might be non-debt liabilities) even if they are also obligations that mature in more than a year.

The second variable we require is shareholders’ equity. The value of shareholders’ equity can usually be found on the balance sheet as well. As a side note, shareholders’ equity is often called stockholders’ equity, owners’ equity, or simply equity. In terms of corporations, all of these terms mean the same thing, which is total assets minus total liabilities. With that said, there may

be very slight variations between shareholders’ equity and equity in some cases.

Long Term Debt to Equity Ratio Example

For example, ABC Company has a long-term debt amount of $102,408 million. Meanwhile, the total shareholders’ equity ratio is $33,185 million. What is the long term debt to equity ratio of ABC company?

First, let’s break it down to figure out the meaning and value of the different variables in this problem.

- Long term debt (in million) = 102,408

- Shareholders’ equity (in million) = 33,185

We can insert the values in the formula and calculate the long term debt to equity ratio:

LTD/E = = 308.60%

In this case, the long term debt to equity ratio would be 3.0860 or 308.60%.

From this result, we can interpret that the value of long-term debt for ABC company is about three times as big as its shareholders’ equity. This seems to be a very high number, considering that other kinds of liabilities are not taken into account. It might seem that the corporation may be taking too much risk. However, to get a more accurate outlook, you may want to compare this result against the industry’s standard as well as the business’ past results.

Long Term Debt to Equity Ratio Analysis

Long term debt to equity ratio can be crucial in determining how risky a business is. For investors and creditors, understanding the proportion of debt, especially long-term, can be a determining factor in deciding whether a business can be reliable to run a successful operation. Remember that some analysts may put more stress on long-term debt. This is because it’s often deemed riskier than short-term debt or current liabilities as a whole.

Unfortunately, there’s no standard number for this ratio. In order to get a solid understanding of how much leverage or risk a business takes, a comparison of the ratio of a particular company against its competitors within the same industry is needed. This aspect is important since companies from different industries have varying standards in the way of coping with their debt.

For instance, capital-intensive corporations (businesses that require large investments in the capital) will most likely have a higher debt ratio compared to companies that are not as assets dependent. On a side note, this doesn’t certainly mean that capital-intensive companies have higher risk as the stability of the cash inflows need to be judged.

One last thing to note is that a low long term debt to equity isn’t always a good indicator. Companies that are hesitant to use debt usually have a harder time to grow their business. As a result, investors won’t get a suitable result in the future. In a different circumstance, low-income companies would naturally have a lower proportion of debt as well to escape bankruptcy. That’s why it’s essential for lenders and investors alike to take advantage of other indicators to make a good judgment.

Limitations of Debt-To-Equity Ratio

When using the debt/equity ratio, it is particularly important to consider the industry within which the company exists. Because different industries have different capital requirements and growth rates, a relatively high D/E ratio may be common in one industry, meanwhile, a relatively low D/E may be common in another. For instance, capital-intensive industries such as auto manufacturing tend to have a debt/equity ratio of over 1, while tech firms could have a typical debt/equity ratio around 0.5.

Utility stocks often have a very high D/E ratio compared to market averages. A utility grows gradually but is usually able to sustain a steady income stream, which allows these companies to borrow very cheaply. High leverage ratios in slow-growth industries with stable income signify an efficient use of capital. The consumer staples or consumer non-cyclical sector most likely have a high debt to equity ratio because these companies can borrow cheaply and have a

relatively stable income.

Analysts are not always coherent about what is defined as debt. For example, preferred stock is sometimes considered equity, but the preferred dividend, par value, and liquidation rights make this kind of equity appear a lot more like debt. Including preferred stock in total debt will increase the D/E ratio and make a company look riskier. Including preferred stock in the equity portion of the D/E ratio will increase the denominator and lower the ratio. It can be a big issue for companies like real estate investment trusts when preferred stock is included in the D/E ratio.

In short, the debt-to-equity ratio can facilitate investors in identifying highly leveraged companies that may cause risks, during rough times. Investors can assess a company’s debt-to-equity ratio against industry averages and other similar companies to gain a general insight into a company’s equity-liability relationship. But not all high debt-to-equity ratios indicate poor business practices. In fact, debt can catalyze the expansion of a company’s operations and eventually produce additional income for both the business and its shareholders.