How To Get Health Insurance Without A Job? Smart ways to cover medical bills

Worrying about how to get health insurance without a job? Read till the end to know about all the valuable insurance and health coverage plans that you can utilize in the absence of employment and health insurance.

Experiencing job loss brings about substantial financial strain, mainly when health insurance is also at risk. You might qualify for a unique enrollment period in the Health Insurance Marketplace if benefits are lost. This special provision enables applying for coverage outside the yearly November open enrollment. Moreover, eligibility for the premium tax credit is likely.

The majority of working-age Americans rely on employer-sponsored health insurance. However, losing a job with this coverage creates a coverage gap. Thankfully, various alternatives exist for the unemployed to secure health insurance during their job search.

Unique insurance options are available to those unemployed, but that requires quick action from you. As you lose your job, you qualify for a “special enrollment” period of 60 days to get health insurance. The U.S. government regulates this special enrollment. However, some private health insurance options are available, which might work fine and come with flexible terms.

Discover the pathways to obtaining health insurance without employment and gain insights into the government and private insurance choices accessible post-job loss.

Health Insurance in America

Health care in the States is costly. A single visit to a doctor can cost several hundred dollars. An average (nothing crucial even) three-day hospital stay might result in tens of thousands of dollars, perhaps even more. The cost of medical care will eventually depend on the type of care you receive, but it will be mind-blowingly expensive in all cases.

Most of us won’t be able to pay such massive sums when we get sick, especially when it’s not in our control- no one knows when they will have an accident or illness. Healthcare is complicated in America, and the only way out is an excellent insurance plan.

Since there is no universal health coverage in the United States, you must manage your health insurance. This is one reason why life is expensive in the States. The way things typically work in insurance is that as a consumer, you will pay an upfront premium to an insurance company, and the insurance company pays your medical bills when the time comes, regardless of the size of the bills.

The premium you pay at intervals makes you share “risk” with many other people who are paying the same premiums. Since it’s unlikely that everyone paying the premiums will suddenly be terminally and critically ill. Most people tend to stay healthy most of the time; the premium money paid to the insurance company is effectively used to manage the expenses of the (relatively) small number of people who get sick or are injured.

Insurance companies are no social welfare companies. They are in this for money, so you can imagine that they study risk extensively. Their goal is to collect enough premiums to cover the medical costs of all members effectively and still make a good profit for the company.

There are several types of health insurance plans in the U.S., regulated by many different rules and regulations regarding money and health care dispensation. Most of the time, healthcare insurance is paid by employers. Healthcare usually comes as an employment benefit.

All companies and businesses with more than 50 employees must include healthcare benefits for their employees and their families. The employers pay all or part of the premiums for the employees’ insurance plans. This is an effective healthcare system that works smoothly until someone loses employment.

Though there is no shortage of private insurance companies, it is always great to have someone (employer) who pays your premiums and protects you in times of illness and injuries.

However, what about when you are out of a job and have no one to cover you against disease and distress?

How do I get health insurance when unemployed?

If you recently lost your job and are worried about your finances and healthcare, you are doing just the most natural thing. There is no universal healthcare coverage in the U.S., and employers fund health insurance plans for their employers. This is why you worry about being ill when you lose your job because the insurance plans may also be terminated along with the job.

To protect the unemployed, quite a few plans help mitigate the situation.

Cobra

The first and most famous one is COBRA. Cobra allows you to keep your previous employer’s insurance plan when you lose your job. It sounds great, but there is a downside too. You are required to pay higher premiums on COBRA, which is when you have already lost the job. This can drain you completely, so you won’t see the benefit of having health coverage at all. If you can pay higher rates, you might as well remain without insurance.

Special enrollment period

Yet another is special enrollment, according to which you can enroll for a new plan after becoming unemployed, but the coverage ends 60 days after the end of your job. This means this option is not helpful for all, as the coverage time is minimal. Sixty days can end very soon, and it is not a time period that most people will find a new job in.

STMs

In some states, short-term health coverage options will be much cheaper and way more attractive than COBRA or the special enrollment offered by the federal government. These short-term coverage plans keep you covered for a year as you seek a new job.

What are the best health insurance programs for the unemployed?

Some private insurance plans help improve things when you can’t get government-supported health coverage.

1- Sidecar Health

Sidecar Health is the best for unemployed people among all the current health insurance programs. It was founded in 2018 and is like a breath of fresh air for health insurance coverage. It’s flexible, affordable, and very approachable, and these characteristics make it the best plan so far.

Pros

- Things work slightly differently with this insurance program. Instead of having an insurance card to show at your doctor’s office, Sidecar Health issues a payment card to pay for your doctor’s visits in cash. This is not just a cheaper and more affordable option; it is also the most flexible and accommodating one.

- Because you are not relying on a health or insurance card and paying from your pocket (using the plan’s benefits), you can visit your doctor at any time. You do not have to follow the restrictions with the provider’s network. Also, you can apply for this insurance whenever you want: there is no need to wait for open enrollment periods when you need one.

- The Sidecar Health insurance is truly amazing; you can apply for it via the internet or even use their smartphone app for the purpose. This means phenomenal ease. Choose your health care deal sitting at home without worrying about paperwork or any other delays. The digital tools of Sidecar Health make it a favorite overall.

- Once on the platform, you have three options to choose from. If you use the standard program, you might as well start with a $0 However, you can always customize your plan according to your needs. Go for custom, and you can set the deductible at $1,000. However, once the deductible is paid, your monthly installments are reduced.

- Sidecar Health comes with very low monthly premiums, which suits those out of a job. In Texas, premium monthly payments start at $215 per month with a $0 deductible for a healthy 50-year-old adult, but you can expect more than $10,000 in annual coverage. This amount may not be much for some people.

- There are no time restrictions regarding getting and canceling the insurance: get it when you want and end it when you don’t.

Cons

- Unfortunately, Sidecar Health won’t be available in some states if you or anyone in the family is expecting a child because its maternity care rider isn’t always available everywhere as per the standard plan. However, maternity and newborn coverage are available with Sidecar’s ACA

- You also should know in advance that registration and approval are a bit complicated. At least, it is more complicated than most other healthcare plans.

- It’s available in just 17 states.

- Healthcare providers’ networks are not part of this insurance plan. The Sidecar plan issues a card that is used to pay for services in cash. There is, most definitely, a limit on the money you can use. Doctors will have their own pricing set for those paying out of pocket and not using the provider’s network services. You will have to ask around for fees before you book an appointment. However, as their registered user, you can use their smartphone app for price comparisons.

2- IHC Group

If you want insurance for a short period that you are out of a job, the IHC Group short-term plan is best for you. They cover you well for a year, and you can utilize that time to look for a new job without worrying about medical bills. If you recently lost your job but are optimistic about landing another one soon, you should go for short-term insurance plans that cover you until you get an employer’s health insurance guarantee.

Pros

- IHC’s short-term plans are best for those looking to fill a temporary gap. The most significant advantage of this insurance plan is that it gives you maximum flexibility for 365 days of the year. You start the plan one day, and it’s effective by the next. No need to wait.

- The annual benefit is quite a lot standing at $ 2 million. This contrasts with the famous Sidecar Health, where annual benefits do not exceed $ 10,000. However, there are no customization offers at the moment, and the yearly benefit cannot be reduced or changed in any way.

- Depending on your state, you can add dental, vision, prescriptions, and telehealth coverage, with riders that start around $25 per month.

Cons

- IHC’s short-term plans come with very high deductibles and monthly payments. When you are out of a job, these payments may be too much for you.

- STM, short-term plans do not comply with ACA, which means free preventive care is excluded from all short-term insurance plans. You should know this before you get one.

- This insurance plan is limited to some states, like many other plans. It’s not available in all states.

- Since STMs or short-term plans are state authority, you can expect many application rules and regulations differences.

3- Blue Cross Blue Shield’s (BCBS)

This is the best among all catastrophic coverage plans for obvious reasons. It is the most economical option among all such programs, perfect for those unemployed. When you are unemployed, you have little inclination to pay high rates for anything, and health insurance

is included. The plan is offered for those young adults below 30 who cannot afford health coverage any other way.

Pros

- The best thing about BCBS is that you can find this plan in all 50 states of the United States.

- The BCBS benefits include ACA compliance means you are entitled to free preventive care under this program.

- Like all other catastrophic programs, the deductibles are high, but the premiums are exceptionally low. This means they are very light on the pocket in the long run.

- A very dedicated program for young adults between 30 and 18.

- It’s a nationwide insurance network, and you can expect quite a lot of uniformity across states.

Cons

- BCBS comes with high deductibles, which may be difficult for some people.

- Coverage policies can vary with the company’s part of the coverage network. This can mean unnecessary complications.

4- Cigna

Cigna insurance programs have access to the nation’s two largest virtual healthcare networks. This means Cigna members have ready access to virtual care, and the best part is that the virtual care facilities are completely free. Virtual care services are a lifesaver for someone experiencing unemployment. Attending the doctor and paying from your pocket can be difficult; Cigna helps you with free virtual care programs.

If you have a query or a problem that may be fixed at home, there you go. Cigna Telehealth has you covered.

Pros

- You can expect Cigna to be present almost everywhere in the States. Its network is vast, with the two largest telehealth networks working with it.

- Telehealth services are free: all plans on Cigna have $0 charges for virtual care.

- Virtual health visits aren’t the only advantage of purchasing Cigna’s health insurance. In-house customer service is available 24 hours daily to answer questions and assist.

- The company also places a $25 monthly out-of-pocket cost limit on insulin regardless of coverage level.

- Dental care starts at around $19, which is marvelous.

Cons

- Cigna Care does not start right after registration; you will have to wait until the first of the following month after registration. This is different from the programs that start the next day after registration.

- Individual plans of Cigna are not available everywhere. They are available in only ten states.

- One real turn-off is the higher-than-average cost of premiums. The monthly installments can be a challenge for some.

5- Oscar

When you lose your job and company-sponsored health insurance, your dependents’ coverage will also be dropped. The entire family will lose the safety net, which can be a huge issue. Things can be more complicated for individuals, but it will be catastrophic for families with no income pouring in regularly. Oscar offers unique features that make life easier for large families after being hit with unemployment.

Pros

- Oscar weaves a safety net for large families who are facing unemployment. With insurer’s plans tax credits, you can reduce your monthly premiums to a significant level. This is especially true if your income is less than four times the federal poverty level.

- Policies put a limit on family deductibles; a family’s overall deductible will not exceed twice the individual deductible, regardless of the size of the family.

- Coverage is easy to acquire with the digital tools offered by the insurance plan. If you get the package online, you get some perks, making the deal even more attractive.

- Use the app to get virtual care or contact the free concierge service staffed by experts who can help you schedule appointments and refill prescriptions. If you sync the app with your smartphone’s step counter, you’ll earn a dollar every day you meet your step goal, up to $100 per year.

Cons

- Oscar coverage is available in only 18 states.

- The provider network is smaller than most other networks.

- Oscar also offers no help for out-of-network visits except in emergencies.

6- Ambetter

Are you looking for the best insurance for dental health coverage? Ambetter is the answer. You can upgrade any Ambetter plan to include dental services for as little as $12 monthly. If you are unemployed, would it not be a hassle and a huge financial burden if you were to buy your dental insurance separately? Yes, it sure will be. This is why Ambetter ranks high among insurance plans for the unemployed.

Pros

- Any Ambetter plan can be upgraded to include dental care for just $12 monthly.

- You can also have your vision care in the plan in some states

- It is one of the cheapest insurance plans out there: this factor makes it a huge favorite among the unemployed because they would like to save every penny until they hit their next jackpot.

- It’s ACA compliant, which means preventive care and medicine are free of cost.

- You choose to live a healthy lifestyle, and Ambetter rewards you for it; this is just a wow factor!

- Teledoctor services are available along with 24-hour nurse services; you no longer have to worry about minor issues.

Cons

- Available in just 24 states, half of America is not eligible.

- There are stringent rules regarding late payments, most likely when you are out of a job. If you fail to pay your premium more than 30 days after the due date, you should immediately say goodbye to the plan.

- The program does not include many digital tools.

7- United Healthcare

Unite Healthcare stands out among other choices with its vast network and comprehensive services. You are never out of the loop with a United healthcare membership. It may not be the absolute best, but you can’t find a match regarding a vast enough network that includes most healthcare providers. You won’t have to check if your current doctor is covered by united healthcare because there is a high chance they will be.

Pros

- An expansive network of more than 3 million physicians and 6,000 hospitals in the U.S. This is more than anyone else can claim.

- You can find UnitedHealthcare’s short-term medical plans in every state. It is, by far. The largest health insurance provider network in the country.

- Dozens of programs and bundles to choose from. You are not restricted to a few ‘pre-planned’ plans.

- These plans are not generally long-term- they are created for people needing insurance temporarily.

- The maximum coverage time on this insurance plan is three years and nothing more than that. The three-year program is in itself an exclusion.

- By adding services like dental or vision, you get good discounts.

Cons

- If we must think of the downsides, it’s the higher premiums than its competitors. However, it must be mentioned that the wonderful tri-term plan is a much cheaper full health coverage and perfect for safeguarding while you are on the new job hunt.

8- Aetna

For those currently unemployed and meeting the criteria for the premium tax credit based on income, Aetna emerges as a compelling choice for health insurance. Notably, every Aetna plan available on the federal marketplace is eligible for comprehensive coverage through tax credits.

Aetna’s prowess in securing the title of “best for premium tax credits” is evident across various evaluations, encompassing domains like affordable health insurance options, coverage tailored for young adults, and plans suitable for self-employed individuals.

A unique advantage for Aetna members is the accessibility to care through CVS’s extensive network of 1,100 MinuteClinic locations across the nation. Many of these services are economically priced or even free, contingent on the specific plan. Additionally, Aetna plan beneficiaries can seamlessly tap into Teladoc’s virtual platform, which offers urgent care, primary care, and mental health services from the comfort of their surroundings.

However, it’s important to note that while Aetna shines when qualifying for the premium tax credit, it might not hold the same cost-effectiveness if this credit doesn’t apply to your situation.

Pros

- For those meeting income-based criteria and currently without a job, Aetna emerges as a standout choice for health insurance. Aetna’s federal Marketplace plans, across the board, qualify for complete coverage through the premium tax credit.

- A unique advantage of being an Aetna member is the comprehensive access to care offered at CVS MinuteClinic locations. With over 1,100 outlets nationwide, these clinics provide a range of services, often at low or no cost, depending on the specific plan.

- Furthermore, Aetna offers an innovative virtual care solution through Teladoc. This encompasses urgent care, primary care, and mental health care services, all accessible remotely. This feature underscores Aetna’s commitment to providing holistic healthcare options that cater to various needs.

- It’s worth noting that while Aetna shines exceptionally when the premium tax credit is applicable, its cost-effectiveness may vary for those not eligible for this credit.

Cons

- ACA gives a localized availability rather than a nationwide reach. This implies that their coverage might be subject to geographical limitations, necessitating careful consideration based on your location and coverage needs.

- It’s worth highlighting that certain bronze plans within the ACA framework come with elevated copayments. While these plans might offer lower monthly premiums, it’s essential to be aware of the potential for higher out-of-pocket costs when seeking medical services. This aspect underscores the significance of evaluating plan details comprehensively to ensure an optimal fit for your healthcare requirements and financial considerations.

9- Molina

Consider Molina’s bronze plan if you’re searching for economical health insurance. Operating in 14 states, Molina offers plans that may not be the most budget-friendly yet feature comparatively modest deductibles. This could translate to reduced out-of-pocket expenses for individuals who frequently utilize their health coverage.

Molina’s health plan members enjoy the added benefit of free virtual urgent care via Teladoc. A user-friendly mobile app complements their services, allowing members to access ID cards, locate in-network doctors, and connect with the nurse advice line.

However, it’s important to note that Molina’s offerings are limited in terms of health management programs, and dental benefits are not included in their policies. Furthermore, the company’s average NCQA plan rating of 2 out of 5 in certain states, which is the lowest among the insurers under review, might impact its overall appeal.

Pros

- Bronze plans from Molina present a noteworthy feature: comparatively low deductibles. This characteristic can reduce out-of-pocket expenses for policyholders who actively engage with their health insurance.

- Molina extends a valuable service by offering virtual urgent care through Teladoc. This innovative approach allows policyholders to access medical consultations remotely, fostering convenience and timely medical attention without needing in-person visits. This can be particularly beneficial for addressing urgent healthcare needs promptly and efficiently.

Cons

- Molina’s offerings encompass a limited range of health management programs, potentially impacting comprehensive wellness support for policyholders. Additionally, their portfolio lacks plans inclusive of dental coverage, necessitating separate arrangements for dental care.

- Operating across 14 states, Molina’s plan availability spans a substantial geographic footprint, providing coverage options to a broad audience. Notably, Molina has the distinction of having the lowest average NCQA rating among the insurers considered. This might influence the perception of their overall plan quality and performance within certain states.

What do you do if you don’t have health insurance?

If you are in the U.S., you won’t leave without health insurance because health coverage is essential to survive here. However, if still, for some reason, you have not been able to get health coverage, and you find yourself unprotected and need medical attention, you should make up your mind about complete out-of-pocket payments.

Medical professionals can even refuse to treat you if any insurance plan does not cover you.

However, U.S. law does not allow hospitals to refuse treatment regardless of your financial situation in case of an emergency.

Additionally, if you genuinely can’t afford coverage, there is always Medicaid. You should check if you qualify for some grants or programs. If even Medicaid is out of the question, you can consider getting a low-cost catastrophic plan for protection.

Where to get health insurance if you are unemployed?

Navigating health insurance options while unemployed offers numerous possibilities. Various insurers are vying for your membership, providing ample choices for an ideal match. Here’s your starting point:

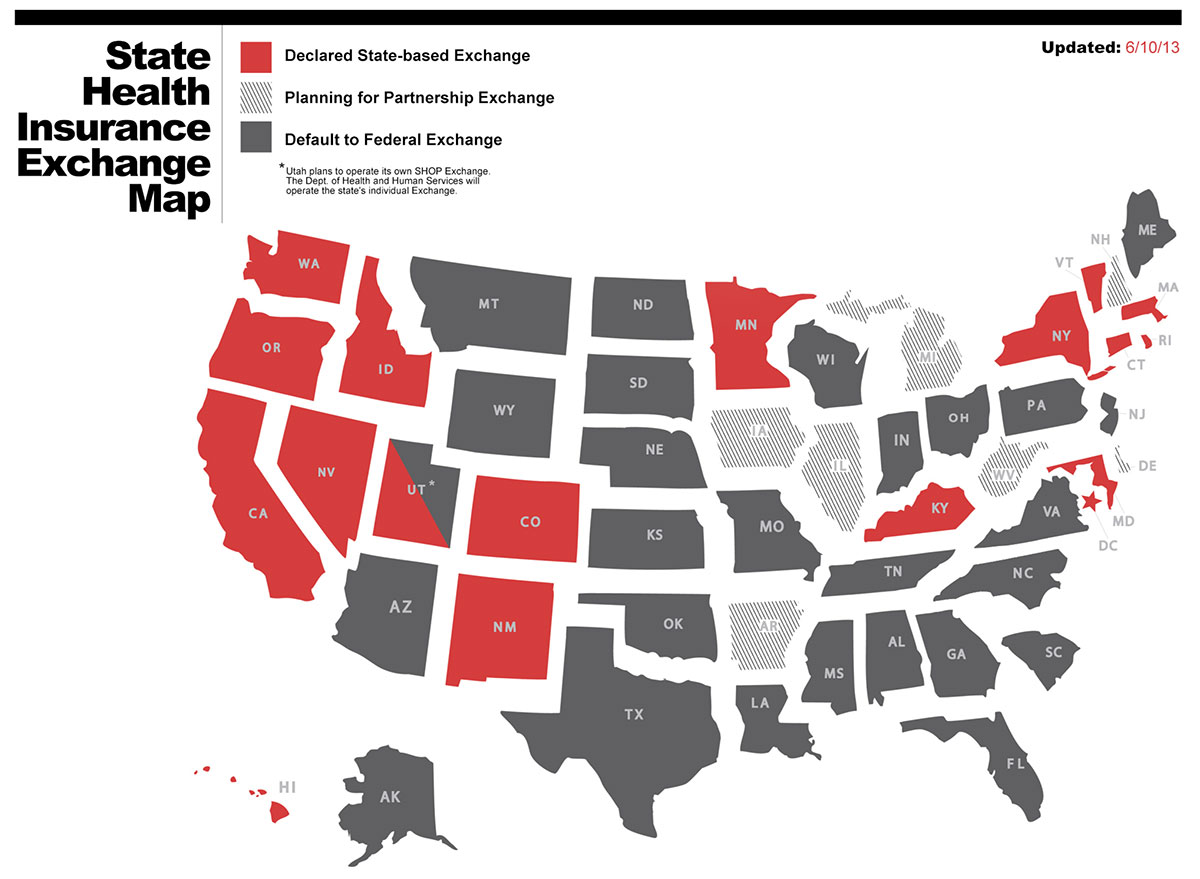

Check out your state’s health insurance marketplace

Begin at your state’s health insurance marketplace. Different states employ different approaches, with some, like Minnesota’s MNsure having dedicated platforms, while others connect via the federal exchange at HealthCare.gov. The rationale for starting here is compelling:

- Diverse insurer selection: Whether through your state’s marketplace or the federal exchange, an array of insurers compete for your attention. This assortment encompasses local, regional, and national companies, each offering an array of plan types.

- Comparability: These marketplaces categorize plans into “metal” levels – Bronze, Silver, Gold, and Platinum. This classification hinges on cost and coverage, not care quality. This makes plan comparisons straightforward, facilitating a genuine “apples-to-apples” assessment.

- Financial relief: Unveiling a crucial reason to prioritize state marketplaces. You might qualify for financial assistance significantly curbing premium expenses. As this aid is exclusive to marketplaces, initially assessing eligibility is advisable.

Direct purchasing from insurers:

Direct interaction with insurance companies becomes essential when seeking health insurance outside marketplaces. This involves visiting insurer websites or engaging with representatives dedicated to the company’s plans.

The benefit lies in obtaining the latest, comprehensive plan details. Insurer websites and advisors are equipped to address a range of inquiries, providing insights into coverage for medical professionals and medications. Sometimes, plans exclusively available through the insurer might not be featured on state or federal exchanges.

These insurer representatives can guide you in selecting a plan by analyzing your past medical costs and usage patterns. This data-driven approach empowers you to make an informed decision aligned with your anticipated future needs. By carefully comparing plans and assessing costs, you can confidently enroll in a plan that suits you best.

Partnering with Health Insurance Brokers for Tailored Coverage:

Navigating the health insurance landscape becomes easier with the help of licensed brokers. These experts act as your personal guides, offering tailored services and access to a broad range of insurers.

Unlike agents tied to one insurer, brokers collaborate with various providers. Their local knowledge helps them recommend plans from both regional and national insurers that suit your community’s healthcare resources.

After identifying the best plan with your broker, they assist you through the enrollment process. They are also available to answer questions and offer support even after you’ve signed up.

Utilizing Internet broker websites:

For those who prefer the convenience of online shopping but lack the time to research individual health insurance companies, internet broker websites offer a compelling solution. These platforms specialize in consolidating plans from multiple insurers, providing a centralized hub for comparison.

It’s important to note that these internet broker websites operate independently from state and federal health insurance marketplaces and cannot offer financial assistance. However, like marketplaces, they facilitate side-by-side comparisons of plans from various insurers.

The platform can facilitate enrollment by identifying the most suitable plan through an internet broker website. However, it’s important to remember that post-enrollment, your interactions and inquiries will be handled by your selected insurance plan, not the broker website.

Enrollment eligibility after coverage loss

If you’ve experienced a recent loss of coverage and intend to secure health insurance through the marketplace, prompt enrollment within 60 days of job-based coverage termination is crucial. Your new plan may activate on the first day of the month following application and enrollment.

Are you anticipating impending coverage loss? Applying ahead of time can help avoid coverage gaps. Should your circumstances change and the new federal health plan becomes unnecessary, cancellation is possible at any point. Do note that cancellation processes may differ for state marketplace coverage, necessitating a review of your plan’s specific cancellation terms.

Options for young individuals:

For those under 26 years old, an alternative solution is feasible. Parents can include you in their existing plan, ensuring continued coverage.

Enhanced assistance for low-income households:

Health insurance might not cover all costs, a challenge during periods of unemployment. However, additional support could be accessible for low-income individuals, including adults, children, pregnant women, older adults, and those with disabilities, through Medicaid or CHIP programs.

Qualification for complementary health insurance or Medicaid hinges on income levels, often below 133% of the Federal Poverty Level (FPL). Eligibility criteria might vary across states, introducing specific rules in some areas.

Differentiating Medicaid and Medicare:

Though sharing similar names, Medicaid and Medicare are distinct programs. Government-backed insurance, Medicaid targets low-income groups like adults, children, pregnant women, older adults, and people with disabilities. On the other hand, Medicare caters to those aged 65 and above, irrespective of income.

FAQs

What are the options for obtaining health insurance if I find myself unemployed?

Two of the top choices for health insurance are Medicaid, which provides insurance at low or no cost, and the ACA health insurance marketplace, offering discounted coverage for eligible individuals. Both programs determine eligibility and expenses based on income, not job status. Thus, although unemployment doesn’t automatically grant eligibility, your income will dictate whether you qualify and at what expense.

Is there any provision for complimentary medical insurance for individuals without employment?

Being unemployed doesn’t inherently grant access to cost-free medical insurance. Nevertheless, public initiatives like Medicaid and CHIP offer free or low-cost insurance solutions for those with limited or no income.

If I decide to leave my job, what is the mechanism behind COBRA insurance?

COBRA insurance maintains the same policy you had while employed. Any progress towards meeting the plan’s deductible remains applicable to the COBRA plan after your departure. Nevertheless, your health insurance expenses will rise since your employer won’t share the monthly plan cost. Typically, COBRA expenses amount to an average of $596 per month.

Can one secure health insurance in the absence of employment?

There are multiple avenues for acquiring health insurance without employment, including ACA marketplace plans, Medicaid, short-term health insurance plans, coverage via a family member, or direct purchase from an insurance provider.

What Does the Health Insurance Marketplace Entail?

The Health Insurance Marketplace is a platform for qualified individuals and families to explore and buy health insurance. This venue simplifies comparing plans, considering factors like premium, out-of-pocket expenses, and plan types. Every program offered through the Marketplace must encompass ten crucial health benefits: hospitalization, emergencies, pregnancy, mental health, and substance abuse treatment.

How Much Does Health Insurance Cost?

The cost of health insurance premiums hinges on individual variables, including your location, age, tobacco usage, plan category (metal tier), and the number of dependents covered. You can reduce your premium expenses if you’re eligible for the advanced premium tax credit. The choice of insurance company also influences the overall cost of coverage.

Can You Explain the Premium Tax Credit?

The premium tax credit is a federal subsidy designed to lower your health insurance premium when you secure a plan through the Marketplace and meet the specified eligibility criteria. To utilize this tax credit, your household income must fall within a specific range, you mustn’t be claimed as a dependent by someone else, and you cannot have the tax status “Married Filing Separately.”

Conclusion

Healthcare costs in the U.S. are high, and we lack a universal, state-funded healthcare system. Although no universal free healthcare policy exists, several supported insurance options can help bridge the gap. Employers are legally required to cover part or all of employees’ premiums, but this coverage typically ends when you lose your job.

During these challenging times, government programs can provide temporary relief. Additionally, consider using multiple private, low-cost health insurance plans to manage your medical expenses effectively.

Explore various coverage options to ensure you have the support you need. With the right combination of insurance plans and government aid, you can better manage healthcare costs and safeguard your financial well-being.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}