Insurance Declaration Page: An Insight Like Never Before

Insurance has become and has been a pivotal part of our lives. An insurance declaration page is one important detail among many others with which one needs to get acquainted to be able to seek better insurance opportunities.

Insurance is a contract in which an individual or entity receives financial protection or compensation from an insurance firm in the form of a policy. The firm pooled the risks of its clients to make payments more reasonable to the insured. Insurance policies are used to protect against the possibility of large and small financial losses resulting from damage to the insured’s property or liability for damage or injury to a third party.

There are many different types of insurance policies to choose from, and almost anyone or any business can find an insurance company eager to insure them—for a fee. Auto, health, homeowners, and life insurance are the most frequent types of personal insurance plans. Car insurance is required by law in the United States, and most people have at least one of these types of insurance.

The firm will offer you a document called a “Declarations Page” when you buy a homeowners insurance policy, renew your policy, or make any modifications to your coverage. The Declarations Page lists the types and quantities of coverage you have, as well as the cost. It is critical that you review the Declarations Page as soon as possible to ensure that it is correct and that you understand what your policy covers. You should notify your agent or insurance provider right away if you see any erroneous or missing information. The sample below may make it easier for you to comprehend your Declarations Page and coverage.

It’s critical to understand the various sections of your insurance policy pages and what they signify to you. The declarations, or “dec” page, which provides a summary of the policy, is the first or one of the first pages you’ll find. The declarations page could be one page or multiple pages long.

Your policy is summarised on the declarations page. A declarations page for a business or personal auto insurance, for example, identifies the named insured and lists the vehicles that are insured, whereas a declarations page for a homeowners or business property policy identifies the named insured and lists the property that is insured. Each renewal term, policyholders should receive a fresh declarations page.

What is insurance?

Insurance is a way of safeguarding against financial loss. It’s a type of risk management that’s generally utilised to protect against the danger of a speculative or unpredictable loss.

An insurer, an insurance company, an insurance carrier, or an underwriter is a company that sells insurance. A policyholder is a person or entity who purchases insurance, while an insured is a person or entity who is covered by the policy. Although policyholder and insured are frequently used interchangeably, coverage can sometimes extend to other insureds who did not purchase the insurance.

In exchange for the insurer’s pledge to repay the insured in the case of a covered loss, the policyholder assumes a guaranteed, known, and generally minor loss in the form of payment to the insurer. The loss might be financial or non-financial, but it must be reducible to monetary terms and usually involves something in which the insured has an insurable interest based on ownership, possession, or a prior relationship.

The insured is given a document, known as an insurance policy, that spells out the terms and conditions under which the insurer would compensate the insured, or their designated beneficiary or assignee.

The premium is the amount of money charged by the insurer to the policyholder for the coverage specified in the insurance policy. If the insured suffers a loss that may be covered by the insurance policy, the insured files a claim with the insurer, which is then processed by a claims adjuster.

A deductible is a mandated out-of-pocket fee required by an insurance policy before an insurer will pay a claim (or if required by a health insurance policy, a copayment). The insurer can reduce its risk by purchasing reinsurance, in which another insurance company agrees to take on some of the risk, especially if the primary insurer considers the risk too great to bear.

What is an insurance declaration page?

The insurance declaration page is a crucial aspect of your policy because it explains:

- The major coverages you have and how much you’ll be reimbursed if you file a claim

- The policy’s various sections have different limits.

- Premiums charged for the coverages you’ve chosen and paid for.

- The person(s) or property(ies) who are covered.

The declarations page usually includes the following information:

- Dates of the start and end of the policy (the policy period)

- Name of the insurance company, the name of the insurance agency, and the name of the policyholder

- Names of individuals or organisations whose interests are additionally protected, such as a bank or credit union (for example, mortgages, business or auto loans), or an extra policyholder

- The policyholder’s mailing address

- The covered property’s or operations’ physical address and a description

- All linked paperwork and endorsements have numbers and dates on them.

- Policy restrictions are measured in dollars.

- Deductible amounts in dollars

- Premium

- If applicable, endorsements (documents that change the policy)

Additional information on the declaration page

Remember that your declarations page is merely a summary of your coverage; it does not contain all of the information contained in your policy.

Information on how to file a claim can be found on some declaration pages. This information should be published in a distinct section of your policy if it is not on the declaration page.

Make sure the declaration page is free of errors. Misspellings, inaccurate coverage levels, or missing endorsements or documents might all impair the coverage of your policy in the case of a claim.

An insurance declaration page’s definition and examples

Your insurance policy includes an insurance declaration page. It’s on the first page of your documentation. It summarises the most important information regarding your insurance.

When you purchase a new vehicle insurance policy, for example, you will be given a declarations page.

Policy declarations page, declarations page are other names for the same thing.

What Is the purpose of an insurance declaration page?

Your insurance policy includes a declaration page. Once your policy is issued, you will receive it. It comes after the insurance binder. It should contain the same information that was supplied to you on the insurance binder.

Despite the name, it could be more than one page lengthy. It could be many pages long, depending on the specifics of your coverage. Every time you purchase or renew an insurance, you should receive a new page.

The insurance binder is a temporary document that spells out your coverage. It can be used as proof of insurance until your policy documents arrive.

Your dec page will be one of them.The dec page is an important component of your policy. It demonstrates:

- The primary coverages that influence how a claim is handled

- What are the restrictions for each section?

- The premiums that are charged

- Who is covered by insurance and what is covered?

The dec page is where you’ll find all of the important details concerning your contract. This covers information such as what is covered and who is insured, as well as how to file a claim and other specifics. You should double-check the dec page to ensure that it is correct.

The following are some of the most common issues seen on insurance dec pages:

- Errors such as a misspelt name or incorrect address

- The improper kind of insurance (for instance, a named perils policy instead of an open perils policy)

- Deductibles that are incorrect

- Coverage amounts that are incorrect

- Riders who have gone missing

- Discounts that aren’t available

The final page should include everything you asked for or agreed to when adopting your new policy. Any mistakes can make it difficult to file a claim. If you find any inaccuracies, please notify your agent so that they can be corrected.

Keep your final page in a safe place once you’ve finished reviewing your policy, as it’s a part of your contract. The policy wording comes after the declaration page. The terminology on the preceding page are defined here, as well as how they apply in a claim. You’ll be able to grasp what each element of your policy implies if you look at the policy wording. It will also explain how it relates to your home.

The main information from your policy will be summarised on an insurance declaration paper. This should include the following:

The policy’s reference number

The policyholder’s name and address

What is covered in an insurance declaration page?

Name, address, and phone number of the insurer.

What kind of coverage is included in the policy?

- Deductibles and limits

- Endorsements

- How long does the policy last?

- Surcharges and discounts

- Insurance premiums are frequently divided into instalments.

- Banks and other designated insureds

- Liability restrictions

On many declaration pages, you’ll find instructions on how to register a claim. This should be mentioned in a separate section of your documentation if it is not on the dec page.

Why do you need an insurance declaration page?

It can be useful to have your insurance dec page readily available in various situations. In some cases, it’s a requirement.

When shopping for insurance, for example, having your dec page on hand makes it simple to compare products. Furthermore, your new insurer will require verification of your current coverage when you switch insurers.

A copy of the final page may also be required if you have a loan on any insured property. Your auto lender, for example, may request it because the dec page will detail what and how much coverage your vehicle has. Your insurance ID card, on the other hand, will not. The lender who is identified as loss payee and/or additional insured on the policy will also be shown on the dec page. The dec page for your homeowners insurance may be required by your mortgage provider.

Your insurer is frequently the one who sends your final document to the lender. However, it is possible that it will be misplaced, in which case you would be required to supply a copy.

The names of those who are involved in the insurance declarations page

The auto insurance declarations page will list all of the policy’s participants. The following people will be involved:

The specified insurance policyholder. Typically, you, the person purchasing the policy to insure your car, are the one who does it. Anyone else who drives the automobile, such as your children or husband, could be the culprit. Each person who is covered by the policy will have their names, ages, and addresses specified. The termination sheet may also include a list of drivers who are not permitted to operate the vehicle.

Drivers who are not allowed to drive. Any drivers in your household who are explicitly excluded from coverage may be included on a dec sheet.

The representative: If relevant, the name and phone number of a representative from your car insurance carrier.

The insurance firm: The address of your insurance carrier, as well as a phone number to contact them, should be included on the policy dec page.

If you leased the car or bought it with a car loan, the lienholder is the business that retains your lease. This is most likely a bank or credit business, and their address may be on the printed sheet.

What is the purpose of an auto insurance declaration page?

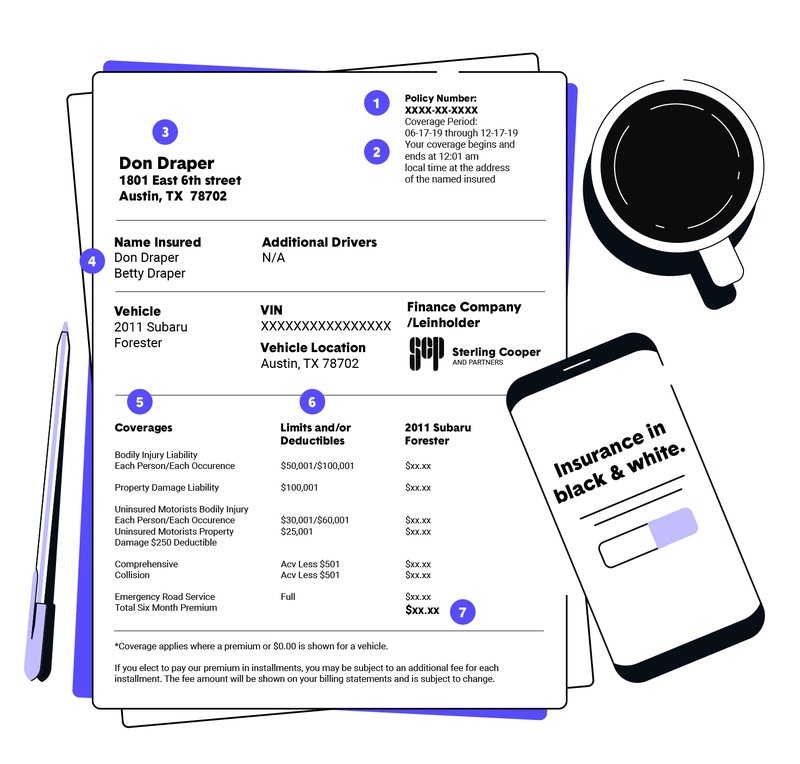

The crucial information concerning your coverage can be found on the declaration page of your auto insurance policy. Consider this page of your policy to be a summary of your coverage. The declaration page contains information about you, such as:

- Policy period: You’ll be able to see when your coverage begins and ends. You can choose between a six-month insurance and a year’s worth of coverage with a long-term policy.

- Drivers: Your auto insurance coverage protects your policy’s covered drivers.

- Vehicles: The declaration page will list the vehicle identification number, make, model, and year of each vehicle covered by your auto insurance policy.

- Loss payees: This is the name of the individual to whom the insurance company will pay claims under the policy.

- Premium: Your automobile insurance premium is another word for the cost of insurance.As a result, the amount of your auto insurance coverage for the policy period will be listed on your declaration page.

- Coverages: You’ll learn about the several types of auto insurance coverages that make up your policy. Insurance coverages such as physical injury and property damage liability, as well as personal injury protection, fall under this category.

- Limitations: Your insurance company’s coverage limits are the maximum amount it will pay out in the event of a loss.

- Deductibles: This is the amount you must pay out of pocket before your insurance coverage kicks in.

- Discounts: Your vehicle insurance company’s declaration page will mention any discounts you qualify for, such as driver training discounts or bundling savings.

Be aware that certain coverage details, such as excluded drivers, will not appear on your declaration page. Your declaration page may or may not include any endorsements you made to your auto insurance policy, depending on your insurer. An automobile coverage declaration web page is the primary web page of your car coverage, and it explains all of the primary information of your coverage, like how good a deal your automobile coverage rates are and the kind of insurance your coverage contains.

You can consider the declarations web page as a precis of your car coverage coverage.Your premium, how often you pay it, and the deductibles you must pay for each coverage component are all listed on the declarations page (also known as the dec page). It will also list your car’s brand, model, and VIN number, as well as the lienholder if you lease.

When will my car insurance declaration page be required?

If you’re buying a car and need to present proof of insurance, you’ll need your auto insurance declaration document. If you’re searching for a new insurer, you can also use your declaration page to compare auto insurance prices.

Where can I get a declaration page for my insurance policy?

If you have coverage through The Hartford’s AARP Auto Insurance Program, you can get a declaration page by contacting us. We understand how essential your time is, so here’s how you can acquire a copy of your declaration page:

Our Customer Service Center is available online.

Call 800-423-6789 for more information.

Is a declaration page insurance proof?

A certificate of insurance, or proof of insurance, is sometimes known as a declaration page. That’s because if you didn’t have insurance, you wouldn’t have a declaration page.

Pages for Other Policies’ Declarations of Insurance From The declaration sheets from Hartford Insurance aren’t just for vehicle insurance. For various types of insurance, you’ll obtain a declaration page, such as:

Insurance for homeowners

Renters insurance is a type of insurance that protects tenants

Insurance for businesses

A homeowners insurance declaration page, like any other insurance declaration page, will have the same policy information as your auto insurance information page.

What should you do with your declarations page after you obtain it?

First, double-check that the information on the policy declarations page is valid. If it isn’t correct, you may have issues when it comes time to file a claim.

When you’ve finished confirming your declarations page, keep it in a safe location alongside the rest of your policy. You may need to refer to it in the future if you need to file a claim or if your policy or carriers change.

What distinguishes a declarations page from an insurance policy?

The declarations page of an insurance policy is part of a much lengthier document called an insurance policy. The DEC page summarises the policy’s main points, whereas the policy itself goes into additional information about terms and provisions.

The premium is the cost of an insurance, which is usually expressed as a monthly cost. The premium is calculated by the insurer based on the risk profile of you or your business, which may include creditworthiness.

For example, if you buy numerous high-end cars and have a history of reckless driving, you will almost certainly pay more for vehicle insurance than someone who owns a single mid-range sedan and has a spotless driving record. For similar policies, however, various insurers may charge varying prices. As a result, doing some research to get the best pricing for you is necessary.

Particular points to consider

People with chronic health concerns or who require regular medical attention should opt for health insurance packages with lower deductibles.

While the annual premium is more than a comparable coverage with a larger deductible, the lower cost of medical care during the year may be worth it.

You can get a copy of your declarations page from your auto insurance company if you don’t have it. You might be able to get it by going to your insurance company’s website or downloading an app. Your insurer should give you a new declarations page whenever you update your coverage or renew your policy.

Premium

The premium is the cost of an insurance, which is usually expressed as a monthly cost. The premium is calculated by the insurer based on the risk profile of you or your business, which may include creditworthiness.

For example, if you buy numerous high-end cars and have a history of reckless driving, you will almost certainly pay more for vehicle insurance than someone who owns a single mid-range sedan and has a spotless driving record. For similar policies, however, various insurers may charge varying prices. As a result, doing some research to get the best pricing for you is necessary.

Premium

The premium is the cost of an insurance, which is usually expressed as a monthly cost. The premium is calculated by the insurer based on the risk profile of you or your business, which may include creditworthiness.

For example, if you buy numerous high-end cars and have a history of reckless driving, you will almost certainly pay more for vehicle insurance than someone who owns a single mid-range sedan and has a spotless driving record. For similar policies, however, various insurers may charge varying prices. As a result, doing some research to get the best pricing for you is necessary.

Optional insurance coverages and declaration pages

Some optional car insurance coverages are available for purchase. These may result in a minor rise in your premium. Some of the vehicle insurance options described above may be considered optional by your auto insurance carrier and indicated as such on your policy declarations sheet. If you lease a car, you may be required to obtain collision and comprehensive insurance by the lienholder.

The following is a list of facts that may normally be found on your insurance declarations page:

- Add-on coverages are normally found on the coverages area of your declarations page, near the middle. Any additional coverages you’ve selected to include in your policy, such as optional sewage and drain backup coverage, will be shown here.

- Limits of coverage: On your homeowners insurance declarations page, you should notice a dollar figure next to each type of coverage in the same middle region. This is the most your insurance company will pay out in the event of a loss that falls under that policy category.

Conclusion

Your insurance policy is essentially a contract between you and the company that insures you. It’s also big and detailed, like most legal documents, but it includes a summary, known as a declarations page in insurance language. This page, also known as a dec page, should be your go-to for key information like the amount of coverage you have on your home, the sorts of endorsements that have been added to your policy, and any discounts you may be entitled for.