State Farm Gap Insurance – The Insurance Your Vehicle Needs

Apart from vintage and collectible automobiles, all automobiles depreciate in value over time. If you've financed your vehicle, you might want to think about gap insurance.

In today’s fast-paced world, owning a vehicle has become more than just a convenience; it’s a necessity for many individuals and families. Protecting your investment is crucial, whether a brand-new car or a reliable used vehicle. That’s where State Farm Gap Insurance comes in – bridging the gap between the actual value of your vehicle and what you owe on your auto loan or lease.

Accidents happen; unfortunately, their financial impact can extend beyond repair costs. When a car is involved in a severe accident or is stolen, traditional auto insurance policies typically cover the actual cash value of the vehicle, which may be significantly less than what you owe. This discrepancy can leave you responsible for paying off a loan or lease on a car that no longer exists.

State Farm Gap Insurance is designed to safeguard you from this financial burden. It provides an extra layer of protection by covering the “gap” between your car’s actual value and the remaining balance on your loan or lease. In the event of a total loss, State Farm Gap Insurance can help save you from being caught off guard by unexpected expenses.

In this article, we will explore the importance of State Farm Gap Insurance, its key features, and how it can provide you with peace of mind in the face of unforeseen circumstances.

What is gap insurance?

Imagine you just bought a brand-new can and are excited about it. But what if your car gets stolen or completely wrecked in an accident just a few months later? That’s where GAP insurance comes in.

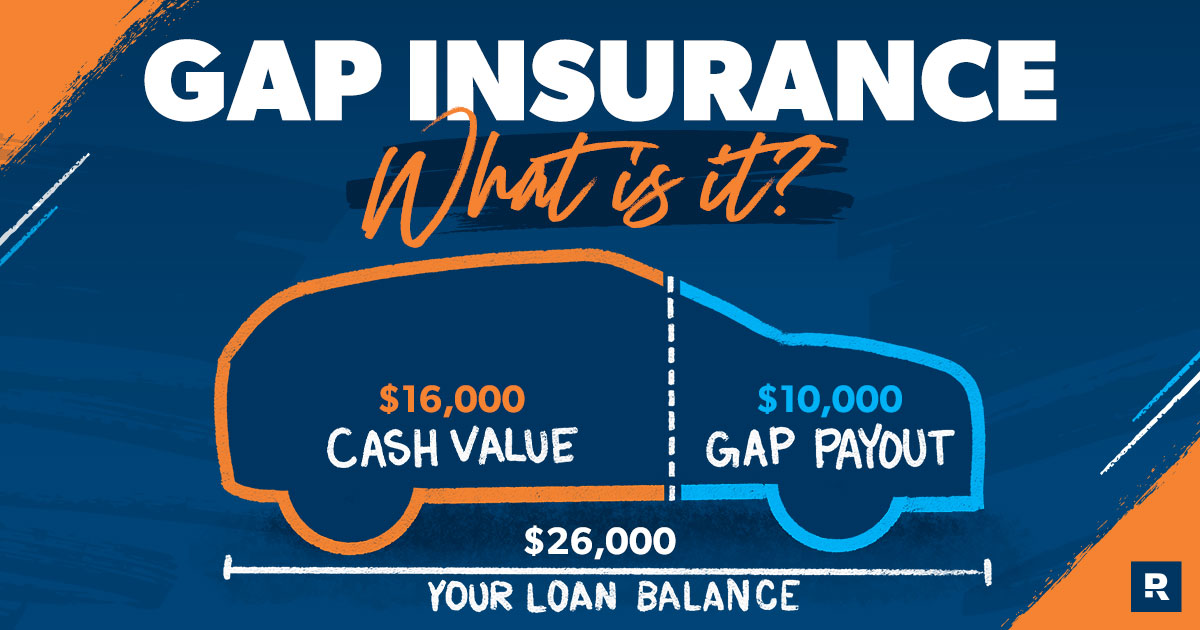

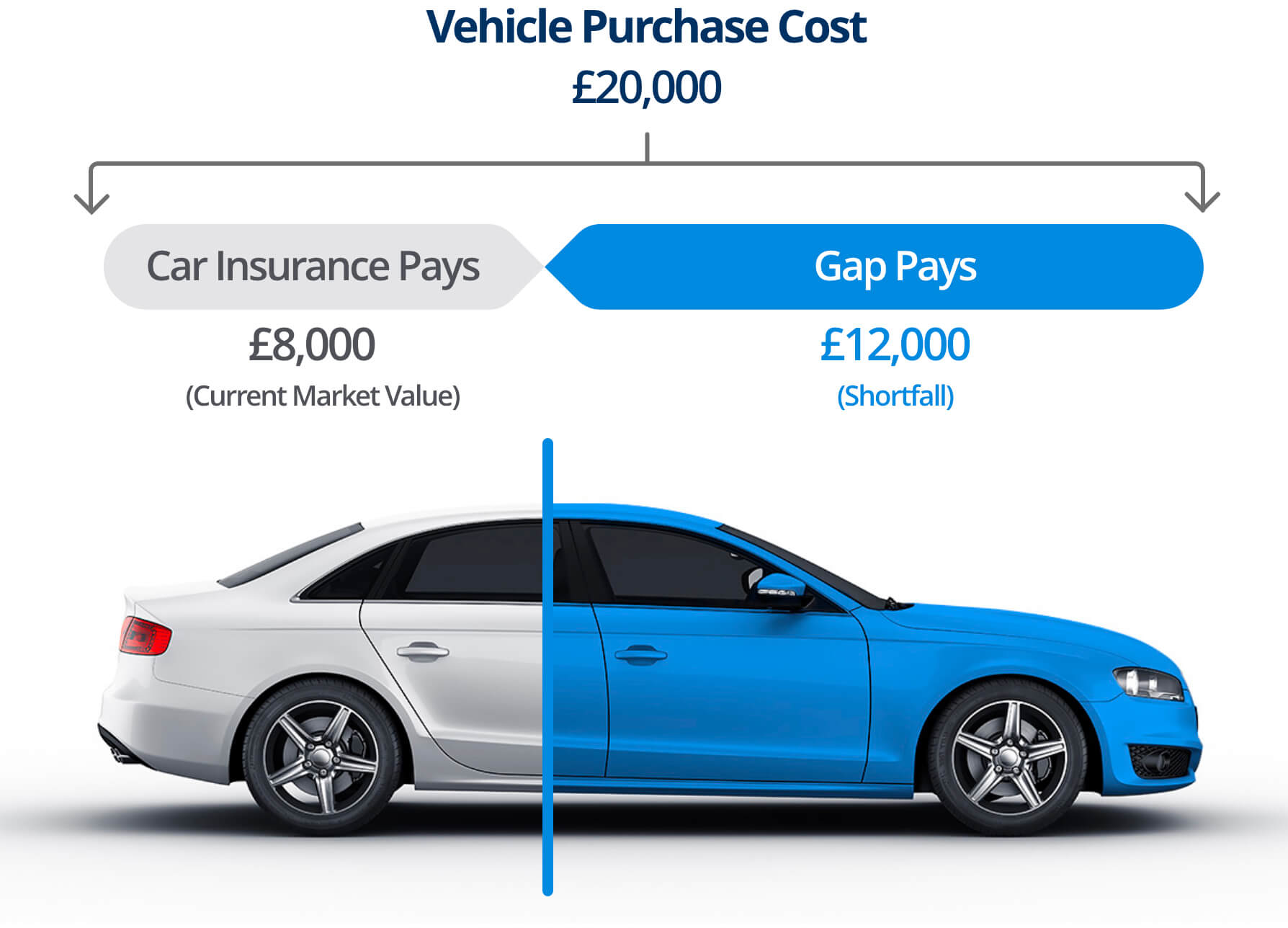

GAP insurance, also known as Guaranteed Asset Protection Insurance, is coverage that helps / protects you financially if your car is totaled or stolen. It covers the “gap” between what you owe on your car loan or lease and the actual cash value of your car.

Here’s how it works: When you buy a new car, its value decreases as soon as you drive it off the lot. However, your car loan or lease may still be for the full amount you paid for the car. So, if something happens to your car, if it gets totaled, the insurance company will typically only pay you the current market value of the car, which may be lower than what you still owe.

That’s where GAP insurance helps bridge that gap between the amount you owe on your car loan or lease and the amount the insurance company is willing to pay you. So, suppose your car is totaled or stolen. In that case gap insurance can cover the difference and ensure that you’re not left with a big financial burden.

Keep in mind that gap insurance is typically optional and may not be required by law or your lender. It’s often recommended for people who have financed or leased a new car with a small down payment, as they are more likely to owe money that the car is worth in the early years of ownership.

It’s important to note that gap insurance usually has certain limitations and conditions, so it is essential to carefully read and understand the policy terms before purchasing it. Suppose you’re unsure whether gap insurance is right for you. In that case, speaking with an insurance professional who can provide personalized advice based on your situation is a good idea.

How much is gap insurance?

The cost of GAP insurance can vary based on a few things. The price depends on factors like the value of your car, how long your loan or lease term is, the deductible amount you choose, and the insurance provider you go with.

Typically, you can pay for GAP insurance in several different ways. You can add it to your monthly loan or lease payments, spreading the cost over time. Or, you can pay for it all at once upfront.

The cost of GAP insurance usually falls within a few hundred dollars, but it’s important to remember that this can vary. It’s a good idea to shop around and compare prices from different car dealerships or insurance companies to find the best deal for you.

Although it might seem like an extra expense, GAP insurance can be a lifesaver in certain situations. Especially if you have a new car and are financing or leasing it, the car’s value can drop quickly in the early years. If your car gets stolen or wrecked during that time, your insurance payout might not be enough to cover what you still owe. GAP insurance bridges that gap and saves you from having to dig deep into your pockets.

Is gap insurance worth it?

Gap insurance is recommended by lenders or auto insurance companies for new vehicles when or if:

- The auto loan has a length of five years or longer

- The loan has a high-interest rate because the principal on the vehicle will take longer to pay down versus the depreciation

- You paid a low down payment, typically less than 20%

Other situations in which gap insurance might not be necessary include:

- When there was a large down payment

- If the initial loan term was short, say three years or less.

You can terminate the coverage anytime, but it’s usually only recommended when the balance due on the vehicle is less than its market worth. Consider the risk cost if you’re unsure if gap insurance is worth it. Gap insurance is relatively cheap and may often be added to an existing full-coverage policy for a small annual fee. That might be a lot less than the gap between the value of your automobile and the amount you repay in the event of a serious accident.

Gap insurance for leased cars

Leased cars, like any other car or SUV, depreciate quickly. Suppose you did not put down much money and still owe a significant amount on your total lease payment. In that case, you will owe more than the vehicle is worth if you get into an accident. Gap Insurance for your lease may be a wise financial move in this circumstance.

To establish if you have a gap, compare your overall cost — including taxes and anything else you folded into the lease — to the vehicle’s MSRP, just like you would with a purchased automobile.

And, just as with a new car, the gap between what you owe and what the car is worth narrows as you make monthly payments and the car depreciates. As a result, you may not require coverage for the duration of your lease. Depending on your leasing agreement, you may only need it for a few months.

What are the benefits of GAP insurance?

When do you need gap insurance?

There is no reason to get gap coverage if your vehicle is not financed. Gap coverage may be a smart idea if you finance your vehicle, but it depends on how much you drive and how rapidly your automobile depreciates.

Keep in mind that automobiles depreciate quickly. According to the Insurance Information Institute, many automobiles depreciate 20% or more in the first year of ownership. If you don’t put down a substantial deposit on a car, the amount you owe in auto payments can quickly exceed the value of the vehicle.

You should consider gap insurance coverage if:

- You made a small down payment

- You have a long financial period

- You drive a lot

- You purchased a vehicle that depreciates quickly

One last thing to keep in mind is that you will typically need to purchase gap coverage while your vehicle is less than three model years old.

Pros and cons of gap insurance

In some cases, gap insurance can provide a significant level of protection, but it is an additional cost to consider. Here are some factors to consider if you are not compelled to get gap insurance but have the option:

Pros

- Gap insurance means you can walk away from an accident with less financial burden.

- You can potentially purchase a more expensive vehicle with less worry.

- The annual cost is relatively low, often $100 or less.

Cons

- At a certain point, the difference between what you owe and the car’s value will drop so that it might not be worth having.

- It is an extra expense for monthly payments and regular upkeep.

- If you pay a low price, to begin with, it might not be necessary.

Which companies offer gap insurance, and how much does it cost?

Gap insurance is available from most major car insurance companies in some form, though many have restrictions on which vehicles they will insure. Geico is the only big insurer that does not provide any gap coverage.

Gap insurance from an insurance company is usually not particularly expensive; thus, we recommend that drivers who would profit from it purchase it.

| Insurer | Does it offer gap insurance? | Limitations |

| State Farm | Yes | It offers a Pay-off protection which means that only vehicles financed through State Farm Bank |

| Progressive | Yes | Up to 25% of actual cash value (lease/loan coverage) |

| Allstate | Yes | It renounces covered losses up to $50,000 and compensates with a deductible payment of up to $1,000. It is offered for new and used vehicles. |

| Esurance | Yes | Up to 25% of actual cash value (lease/loan coverage if you have full coverage insurance) |

| Farmers | Yes | New vehicles only |

| Travelers | Yes | Offering loan/lease coverage pays out the difference between your car’s current value and what is owed. |

| Nationwide | Yes | Offers GAP insurance but does not waive the deductible. |

| 21st Century | Yes | Only available in AZ, CO, ID, IA, KY, MT, NM, OR, NE, TN, UT, WA, and WI |

| USAA | Yes | Only vehicles financed with a USAA auto loan. |

| Geico | No | — |

| American Family | Yes | Traditional GAP policies |

| Safeco | Yes | Traditional GAP policies |

How much does gap insurance cost?

According to the Insurance Information Institute, auto insurers normally charge a few dollars per month or roughly $20 per year for gap insurance. Various criteria, including the worth of your vehicle, determine your cost. You’ll also need to purchase collision and comprehensive coverage. Compare auto insurance prices from at least three companies to find the best one.

According to United Policyholders, a nonprofit consumer group, lenders charge a fixed premium of $500 to $700 for gap insurance, though credit unions may charge less.

Remember that if you add coverage to your loan, you’ll also have to pay interest. According to Edmunds, the average financing rate on a new automobile is about 6%. This means that three years of gap coverage from a dealer might cost over $800 versus $60 from your auto insurer.

Prices and interest rates vary, so compare prices with your dealer and car insurance provider.

How is gap insurance calculated?

Lenders and dealers figure out how much gap insurance would cost you depending on your loan and the estimated depreciation of your vehicle. For larger debts, gap insurance can be more expensive. Car insurance providers figure out how much gap insurance will cost you depending on your vehicle and driving history.

Does gap insurance always payout?

Only if your complete loss claim is approved and the settlement you receive for your vehicle does not cover your outstanding loan does gap insurance kick in. Gap insurance can also pay the difference between their insurance company’s settlement offer and the outstanding debt if another driver is at fault.

Some gap insurance policies have a cap on how much you can get. For example, Progressive’s gap insurance policy covers up to 25% of the vehicle’s ACV. If your car has depreciated significantly, this gap payment may not be enough to cover the entire loan.

State Farm – The place you should buy your gap insurance from

State Farm, the nation’s largest vehicle insurer, does not offer gap insurance, but it does have a feature called Pay-off Protector that anyone who gets a car loan from a State Farm bank (a partnership with US Bank) is eligible for. Pay-off Protector is only applicable to full-coverage vehicle insurance, although it is not required that State Farm underwrite the policy. If your loan is from State Farm, you are eligible for Pay-off Protector at no additional cost, even if a different insurance carrier writes your motor insurance policy.

How much is State Farm car insurance?

According to our annual survey of the Cheapest Car Insurance Companies, most drivers can save money with State Farm. State Farm had an average auto insurance rate of $1,168. After USAA and Geico, this is the third-lowest average rate in our survey. This pricing also indicates savings compared to our study’s national average rate of $1,320.

Remember that your auto insurance premiums will vary depending on your unique circumstances. Even though State Farm has some of the best rates, our research discovered a few outliers for certain demographic groups.

State Farm has various categories for auto insurance rates, with rates that are up to 15% less than the national average. These categories include:

- State Farm rates for teen drivers

- State Farm rates for young adults

- State Farm rates for seniors

- State Farm rates for drivers with poor credit

- State Farm rates for good drivers

- State Farm rates after a speeding ticket

- State Farm rates after an accident

- State Farm rates after a DUI

How much is high-coverage car insurance with State Farm?

While the national average rate for high coverage is around $1,397, State Farm offers an insurance rate of $1,256 for high-coverage car insurance.

So, if you’re seeking insurance with additional coverage, State Farm is near the top, according to our research, of our list. Only two competitors, USAA and Geico, have lower average rates for this type of coverage.

How much is the minimum coverage car insurance with State Farm?

On the other hand, the national average for minimum coverage is coverage car insurance is $1,248, and State Farm offers the same for $1,086. A stellar difference, isn’t it?

State Farm, as per our research, is one of the more affordable auto insurance carriers for consumers looking for a basic policy. USAA leads the pack in this category, with Geico coming in second, although State Farm is a decent option for most other drivers.

State Farm car insurance discounts

Customers and potential customers of State Farm can save money on their insurance by qualifying for one or more discounts. State Farm offers incentives similar to those offered by the top auto insurance providers in our rankings, such as discounts for good students and accident-free drivers. State Farm, for example, offers two opt-in, app-based safe driving programs. If the software recognizes a trend of safe driving habits, it may result in discounts.

Steer Clear is a safe driving program for policyholders under the age of 25 that uses an app. Remember that discounts vary by state, so policyholders should always check with State Farm, according to our research, only to see if they are eligible.

- Student/Good student

- Student away from home/storage

- Bundling/Multi-policy

- Multi-vehicle

- Good driver/Clean record

- Defensive driving course

- New car/Safety/Anti-theft equipment

- Low mileage

- Tracking device program

What is the insurance code for State Farm?

At State Farm, privacy and security are valued, and a variety of measures are used to protect personal identity. A 10-digit code called a key code is developed to facilitate quick identification of your current bill. Each time a new bill is generated, State Farm creates a new key code to be associated. The key code doesn’t provide anyone access to your information, account, or policies. The key code is only used for making a one-time insurance payment over the phone or online.

Frequently asked questions

How do I get the best deal on gap insurance?

Gap insurance can be purchased through a dealership, a traditional vehicle insurer, or a specialty gap insurance business.

For some drivers, dealership-based gap insurance coverage is too pricey to justify, even if it is a convenient choice. Shop around at the dealership, vehicle insurers, and gap insurance businesses; your greatest offer might come from your current car insurance provider. If you already have comprehensive coverage, gap insurance may be available for a small annual fee.

Do you get money back from gap insurance?

You may be entitled to a reimbursement of the unused amount of your gap insurance if you pay off a vehicle loan early. Some jurisdictions require insurers to repay premiums if a 36-month loan with 36-month gap coverage is paid in 24 months.

In rare situations, an insurer may fail to notify you if you are eligible for a refund. Always keep your payback letter, the original contract or insurance paperwork, and an odometer disclosure statement with you. Before purchasing gap insurance, it is critical to understand an insurer’s refund policy. It may be beneficial to contact your state’s commerce department or insurance commissioner’s office beforehand to learn about your state’s regulations or what to do if your insurer fails to meet your expectations.

How does gap insurance work if your car is totaled?

Only the difference between the real cash value of a car at the time of a complete loss claim and the current amount still outstanding on an auto loan is covered by gap insurance. Total loss can differ depending on state law and/or insurance provider.

Do I need gap insurance if I have full coverage?

While you may believe your auto insurance coverage is comprehensive, most motor insurers do not offer a single “full coverage” policy meant to protect you against every eventuality. Instead, combining several forms of coverage (e.g., liability, collision, and comprehensive) can provide more protection. Adding gap insurance to existing coverage can provide some drivers with additional peace of mind. However, each driver’s coverage requirements and benefits will differ significantly.

What is the highest amount of money that GAP insurance will pay?

GAP insurance only covers the difference between the insurance car’s value and the total amount of the loan. GAP insurance does not cover more than the loan’s remaining amount.

Can we get a refund on GAP insurance?

You can not get a refund on covered but only on premiums. For example, if you paid 7 months of coverage but then canceled on one, you can get a 6 months refund on premiums. You can not get a refund for the one month you had coverage.

How will GAP insurance work if my car is totaled?

If your car is totaled and the insurance payout is less than the remaining balance on your loan or lease, gap insurance steps in to pay off the remaining amount. This helps to protect you from being financially responsible for a vehicle you will no longer possess.

The bottom line

When it comes to safeguarding your vehicle with gap coverage, options abound. While dealerships offer this protection, opting to include it in your existing policy generally proves more cost-effective. Don’t hesitate to explore quotes from leading insurers for a clearer picture of potential rates. Interestingly, although State Farm doesn’t provide conventional gap insurance, their auto insurance packages promise greater savings on premiums compared to many other gap coverage alternatives.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}