What Does APR Stand For?

What does APR stand for, and how does it work? Give this article a thorough read to find out.

You’ll see that APR is utilized related to a few distinctive monetary items, including credit cards, loans, and recruit purchase arrangements. But have you ever wondered, what does APR stand for and how can it function? In this article, we will disclose all that you need to know about Annual Percentage Rates.

What does APR stand for?

APR stands for Annual Percentage Rate. It is the official interest rate utilized for borrowing on a credit-based item. In addition to this, APR considers the rate of interest you’ll pay together with any extra charges or fees. All in all, it’s a common method of showing the expense of acquiring longer than a year.

The expression “annual percentage rate (APR)” alludes to the annual rate of interest charged to borrowers and paid to financial backers. APR is communicated as a percentage that addresses the actual yearly expense of assets over the term of an advance or a payment acquired on investment. This incorporates any fees or extra expenses related to the exchange. However, it doesn’t consider compounding. The APR furnishes customers with a bottom-line number which they can undoubtedly use to contrast rates from different banks.

The APR will be communicated as a percentage of the sum you’ve acquired and is determined by utilizing an equation laid out in the Consumer Credit Act (1974). Every bank should keep this, making it a valuable method to think about items, for example, loans and credit cards on a like-for-like premise. Notwithstanding, note that the APR will just consider mandatory charges, which implies that avoidable fees like those for late installments or going over your credit limit won’t be incorporated.

Suppose you borrow $10,000 over a span of 3 years to purchase a vehicle. An APR of 5.5% would incorporate your annual interest rate together with any standard fees payable for the advance. You would then compensate for 36 month-to-month reimbursements of about $301, adding up to $10,848.60. This incorporates the $10,000 you acquired and $848.60 in interest and fees. Your reimbursements are similar consistently on account of how the interest is determined. In addition to this, toward the beginning of the credit term, your reimbursements will incorporate more interest but less of the advance balance. Towards the end of the credit term, your reimbursements will incorporate less interest but a greater amount of the loan balance.

How does the Annual Percentage Rate (APR) work?

An annual percentage rate is communicated as an interest rate. It ascertains which percentage of the principal amount you’ll pay every year by considering things like regularly scheduled installments. APR is additionally the annual rate of interest paid on investments without representing the building of interest within that year.

The Truth in Lending Act (TILA) of 1968 ordered that loan specialists reveal the APR they charge to borrowers. Credit card organizations are consistently permitted to publicize interest rates. However, they should unmistakably report the APR to clients before they consent to an arrangement. Furthermore, APR is utilized for looking at credit cards and unstable loans and is communicated as a percentage of the sum you’ve acquired. For instance, an individual loan with a 15% APR ought to be less expensive than one with a 17.5% APR, although you ought to consistently check the agreements.

In addition to this, you must remember that it is important for an APR to just incorporate obligatory charges. A few fees, like installment security, may not be considered, so you should consistently pursue the agreements cautiously prior to applying for credit. APR likewise doesn’t cover any fines for being late with installments or going over your credit limit. Let us now look at an example as to how an APR works

On the off chance that you acquire $1,000 on a credit card with a 12% APR (and you don’t reimburse any of the obligations), it will cost you $120 in interest throughout the span of a year. The APR is typically added to your debt consistently. To track down the month-to-month interest rate, divide the APR by 12. The month-to-month rate on a 12% APR is 1%. In the event that you owe $1000, you will be charged $10 interest every month. Moreover, if the period over which you spread your reimbursements is longer, the month-to-month cost will be lower. However, the general interest paid would be high.

How Is APR calculated?

The rate is determined by increasing the intermittent interest rate by the number of periods in a year in which the occasional rate is applied. It doesn’t demonstrate how frequently the rate is applied to the balance. The formula to calculate APR is:

APR=((Fees +Interest Principal/ n)×365)×100

where:

Interest=Total interest paid over the life of the loan

Principal=Loan amount

n=Number of days in the loan term

In America, an APR is commonly introduced as the intermittent interest rate multiplied by the quantity of accumulating periods each year. On the other hand, the concept of APR might be very unique outside of the United States. The European Union (EU) centers around buyer rights and monetary straightforwardness in characterizing this term. Moreover, a solitary equation for computing interest rate was set up for all EU part countries. This has been done despite the fact that individual nations have some elbow room over deciding the specific circumstances in which this formula is to be considered in EU-specified cases.

Types of APRs

Credit card APRs differ depending on the charge. A loan specialist may charge one APR for purchases, another for loans, but another for balance transfers from another card. Likewise, banks charge high-rate punishment APRs to clients for late installments or disregarding different terms of the cardholder arrangement. There’s likewise the starting APR — a low or 0% APR — which many credit card organizations use to tempt new clients to pursue a card.

The APR borrowers are charged also on the basis of their credit. Advances offered to those with incredible credit carry altogether lower interest rates than the rates accused to those of terrible credit. Therefore, you must know the sort of APR on your credit. Most of the time, you’ll either have a fixed APR or a variable APR.

A fixed APR loan has an interest rate that is ensured not to change during the existence of the loan or credit office. A fixed APR implies the APR doesn’t change depending on a record during the existence of the credit. Along these lines, fixed APRs can be more unsurprising concerning planning. Regular instances of credits with fixed APRs incorporate most home loans and individual loans.

On the other hand, a variable APR loan has an interest rate that may change at any time. Variable APRs can change and are attached to a file interest rate, for example, the excellent rate distributed in the Wall Street Journal. So if the superb rate increments, so would a variable APR. Furthermore, variable APRs can vacillate either in support of yourself or against it. So while a variable APR might actually give lower interest rates forthright, it can likewise increment as the related list expands, which is a disadvantage of variable APRs. You’ll regularly see this kind of APR on credit cards.

What’s the difference between an APR and an interest rate?

Interest rates and APR are two frequently confused terms that allude to similar ideas. However, there are unpretentious differences with regards to estimation. While assessing the expense of a loan or credit extension, comprehend the distinction between the publicized interest rate and the annual percentage rate (APR), which incorporates any extra expenses or fees.

The interest rate is essentially the sum charged on the amount you borrow. It is communicated as a percentage and is generally cited annually. An APR, then again, incorporates the rate of interest, in addition to some other fees, making it a more genuine portrayal of the all-out cost of the item.

The advertised rate, or ostensible interest rate, is utilized while ascertaining the interest cost on your advance. For instance, on the off chance that you were thinking about a home loan credit for $200,000 with a 6% interest rate, your annual interest cost would add up to $12,000, or a regularly scheduled installment of $1,000.

The APR, be that as it may, is the more viable rate to think about when contrasting credits. The APR incorporates the interest cost on the credit as well as all fees and different expenses associated with securing the advance. These fees can incorporate broker fees, closing expenses, refunds, and rebate focuses. These are regularly communicated as a percentage. Moreover, the APR ought to consistently be more noteworthy than or equivalent to the ostensible interest rate, with the exception of a specific arrangement where a loan specialist is offering a refund on a part of your interest cost.

What is a representative APR?

APR can help you look at loaning items, for example, advances or credit cards, on a like-for-like premise. In the event that you look for an advance, say on a value examination site, the distinctive credit alternatives are frequently positioned by representative APR. At the point when an advance or credit card is promoted with a representative APR, the rate should be offered to basically 51% of aspiring candidates for the item. In any case, this implies that the other 49% may not be qualified for the publicized rate and are probably going to pay more.

The piece of information is in the word ‘representative’. At the point when credit is promoted with a representative APR, it implies that essentially 51% of clients get a rate that is equivalent to, or lower than, the representative APR – albeit not every person within the 51% will fundamentally get a similar rate. It may very well maybe not be difficult to accept that the bank with the minimum representative APR you discover will give you the best rate. In any case, when you apply, it’s a possibility that you’ll get an individual APR dependent on your conditions. This could be something similar, higher, or lower than the representative APR.

What is a personal APR?

At the point when you apply for a loan, all things considered, the rate you get will be based on your personal conditions. It will take into account your credit history and funds, just as the credit sum and length of your borrowing. This is your own APR. All in all, an individual APR is a rate you’re really given, and it will be founded on your personal conditions just as the sum you need to acquire.

Understand this before you apply – especially in case you’re looking dependent on the representative APRs you see promoted. The representative APR is a helpful examination instrument, however not the rate you’ll get. For sure, all things considered, clients will get an individual APR regardless of whether they are in the 51% who get a rate that is equivalent to, or lower than, the representative APR.

You probably won’t have a clue about your personal rate until after you’ve applied for an advance, and essentially applying could influence your credit rating. This is on the grounds that moneylenders will ordinarily check your monetary foundation with a credit reference organization before concluding whether to make you an advance offer, and the checks will be recorded on your document. When you apply for a line of credit, the loan specialist needs to refresh your credit record.

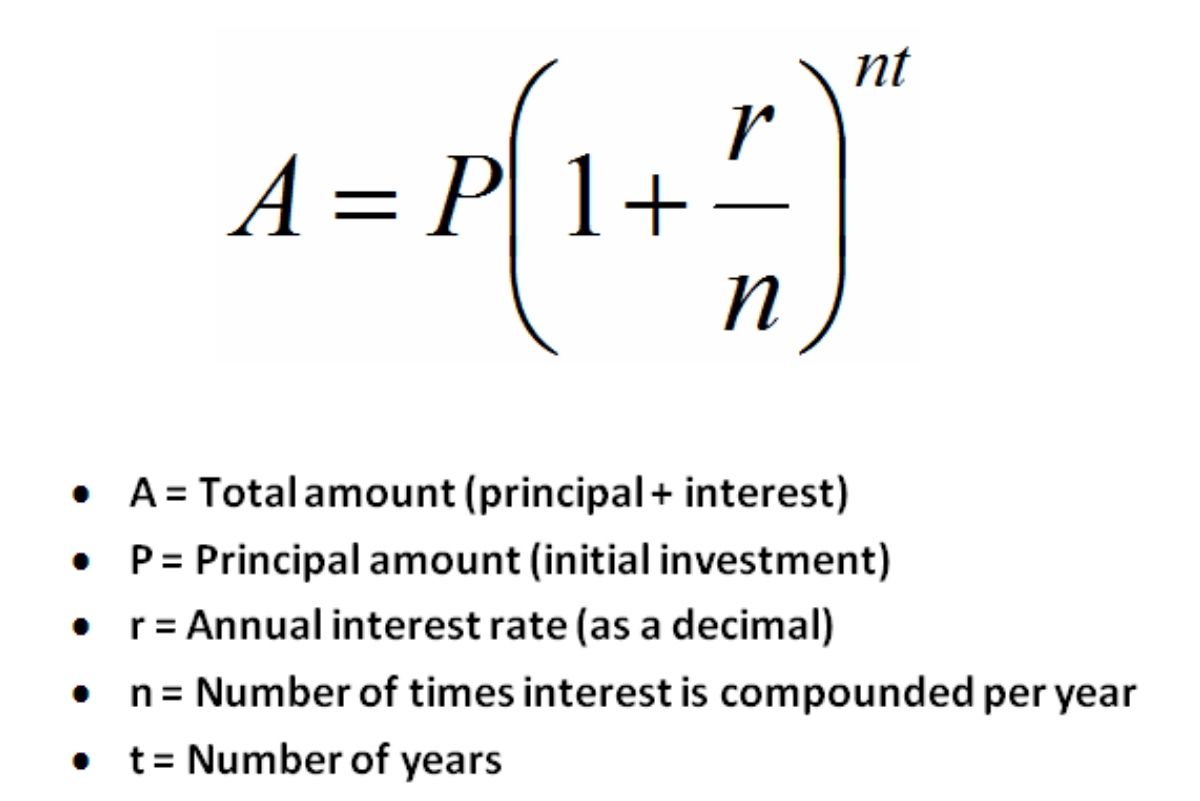

APR vs. Annual Percentage Yield (APY)

While an APR just records for basic interest, the annual percentage yield (APY) considers accumulating interest. Thus, a credit’s APY is higher than its APR. The higher the interest rate, and the smaller the compounding time frames, the more prominent the distinction between APR and APY.

Envision that an advance’s APR is 12%, and the credit intensifies one time per month. On the off chance that an individual gets $10,000, their interest for one month is 1% of the total or $100. That viably expands the surplus to $10,100. The next month, 1% interest is evaluated on this sum, and the interest installment is $101, marginally higher than it was the earlier month. If you convey that equilibrium for the year, your viable interest rate becomes 12.68%. APY remembers these little moves for interest expenses because of accumulating, while APR doesn’t.

Here’s one more approach to take a look at it. Let’s assume that you think about an investment that pays 5% each year with one that pays 5% month to month. For the main, the APY approaches 5%, equivalent to the APR. However, for the second, the APY is 5.12%, mirroring the month-to-month compounding.

Given that an APR and an alternate APY can be utilized to address a similar interest rate, it makes sense that loan specialists and borrowers will underline the seriously complimenting number to express their case, which is the reason the Truth in Savings Act of 1991 ordered that the two APR and APY be unveiled in promotions, contracts, and agreements. A bank will publicize an investment account’s APY in an enormous textual style and its relating APR in a more modest one, given that the previous highlights a cursorily bigger number. The inverse happens when the bank goes about as the loan specialist and attempts to persuade its borrowers that it’s charging a low rate. An extraordinary asset for contrasting both APR and APY rates on a home loan is a home loan calculator.

What is an APRC?

APRC represents the Annual Percentage Rate of Charge and is the interest rate related to contracts and borrowed loans. Different from credit cards, where you might be offered a higher APR if your credit score isn’t sufficient when you apply for a home loan, you’ll just be turned down on the off chance that you don’t meet the loaning examples. This implies that, in contrast to an APR, the APRC doesn’t change. In the event that you are acknowledged for a home loan, you’ll as a rule pay an early on rate for around two to five years, before the rate returns to the bank’s standard variable rate.

The APRC factors in both of these rates, and shows you the complete expense of a home loan, including fees, over the full length of the credit – frequently 25 years. All in all, it shows you how much your home loan would cost you if you somehow managed to remain on a similar home loan until you had reimbursed the sum acquired. Moreover, in any case, if you intend to change to another home loan when your initial arrangement closes, you don’t have to stress over the APR.

What is APR on a credit card?

APR ought to be promoted on all acquiring items, from credit cards and advances to contracts. As a component of industry guidelines, all moneylenders compute APR the same way. To make it simpler to analyze loan items, APR considers any extra fees and how regularly you’re charged with interest. APR is an annualized portrayal of your interest rate. Furthermore, when choosing credit cards, APR can help you think about how costly an exchange will be for everyone. For the most part, credit card organizations offer a grace period for new items bought. On the off chance that you just make buys and take care of your closing balance every month by the due date, you simply pay the sum you owe with no interest. Nonetheless, in the event that you select to convey an equilibrium on your card, you pay the interest that is decided on your extraordinary equilibrium.

Can APR help me calculate how much I’ll pay?

Computing the amount you’ll pay every year can get somewhat muddled, particularly with regards to credit cards. This is on the grounds that credit cards have adaptable reimbursements (for example you can repay more in one month than another if you pay at least the base sum), and your supplier will for the most part ascertain interest on a month-to-month or regular schedule. Thus, the measure of interest you pay annually relies upon how your balance changes over the course of the year. For instance, in the event that you reimburse your credit card balance in full and on time each month, you will not pay any interest whatsoever – regardless of what your APR is. Along these lines, APR can be a decent method to analyze credit cards, however, recollect that what you really pay in interest relies upon how and when you take care of your obligation.

What affects your APR?

The APR you’re offered by a bank will rely upon your credit score and how well you’ve acquired previously. If you’ve generally reimbursed obligations on schedule and haven’t surpassed your credit limit, you’ll be offered a more serious APR than somebody who has consistently missed installments and is in this way seen as a more serious danger. Moneylenders will likewise take a look at your annual compensation and family spending prior to choosing what APR to offer. The sum you need to get and the time allotment you need to get for will likewise be considered. For individual credits, you’ll generally track down that the more you need to acquire and the more drawn out the term, the lower the APR will be. In any case, you ought to consistently guarantee you’re just acquiring what you can bear to repay.

Why should I be careful about not making too many credit applications?

Each time you apply for credit, the loan supplier plays out a hard credit check. This leaves an imprint on your credit record. Loads of utilizations can make you look desperate for credit. It is hasty to apply for too many credit items simultaneously. To get the representative APR, you may need to meet certain conditions and credit score standards. To perceive what you could get dependent on your conditions, consistently read the important part first. Check your credit report before you apply for credit. You may have to further develop it to be qualified for the top credit items. You’re bound to be offered the promoted APR on the off chance that you have a decent credit rating. A lower APR is an extraordinary inspiration to further develop your credit score.

What is a good APR?

What considers a “good” APR will rely upon variables, for example, the contending rates offered on the lookout, the excellent interest rate set by the national bank, and the borrower’s own credit score. At the point when prime rates are low, organizations in cutthroat ventures will once in a while offer extremely low APRs on their credit items, for example, the 0% APRs here and there offered on vehicle advances or rent choices. Although these low rates may appear to be alluring, clients ought to check whether these rates keep going for the full length of the item’s term, or regardless of whether they are essentially basic rates that will return to a higher APR after a specific period has passed. Also, low APRs may just be accessible to clients with particularly high credit scores.

The lower the APR the less you will pay in interest and different charges. Many credit cards offer 0% APR on buys and balance moves for a set number of months. Be that as it may, check what the APR will return to after this point as this is the rate you’ll cover on the off chance that you don’t take care of your equilibrium inside the 0% period. Other serious credit cards offer low APRs of around 7.9% to 9.9% APR.

Cutthroat individual credit rates are around 2.8% to 4.9% APR for advance sizes of somewhere in the range of $7,500 and $20,000. On the off chance that you need to get pretty much more than this sum, your APR is probably going to be higher. It’s in every case best to search around and analyze your alternatives cautiously prior to applying for a credit card or individual advance. Numerous banks offer qualification checkers which will give you a sign of the fact that you are so prone to be acknowledged for a specific credit card or advance. Qualification checkers run a ‘soft’ search on your credit document, so it will not leave an imprint on your credit record for different moneylenders to see. On the off chance that there is a great deal of ‘hard’ searches on your credit document in a short space of time, banks may consider this to be a sign you’re attempting to get credit.

Conclusion

What does APR stand for? Since you have perused this article, you thoroughly understand APR and what it implies. APR, or annual percentage rate, is your interest rate expressed as a yearly rate. An APR for credit can incorporate fees you might be charged, similar to beginning fees. APR is significant in light of the fact that it can give you a good idea of the amount you’ll pay to apply for a new line of credit.