What Is Considered An Excellent Credit Score?

Before taking a look at what is considered an excellent credit score, we first need to understand what ‘credit score’ actually is. As a rule, a credit score is a three-digit number going from 300 to 850. Financial assessments are determined utilizing data in your credit report, including your payment history; the measure of obligation you have; and the length of your record of loan repayment.

There are a wide range of scoring models, and some utilization of other information in ascertaining credit scores. These credit scores are utilized by possible moneylenders and creditors, for example, banks, credit card organizations or vehicle sales centers, as one factor when concluding whether to offer you credit, similar to a loan or credit card. It is one factor among numerous to assist them with deciding that you are liable to pay back cash they loan.

Remember that everybody’s monetary and credit circumstance is unique, and there is no “magic number” that may ensure better loan rates and terms. So let us head straight into the article and learn more about credit scores.

What Is Considered An Excellent Credit Score?

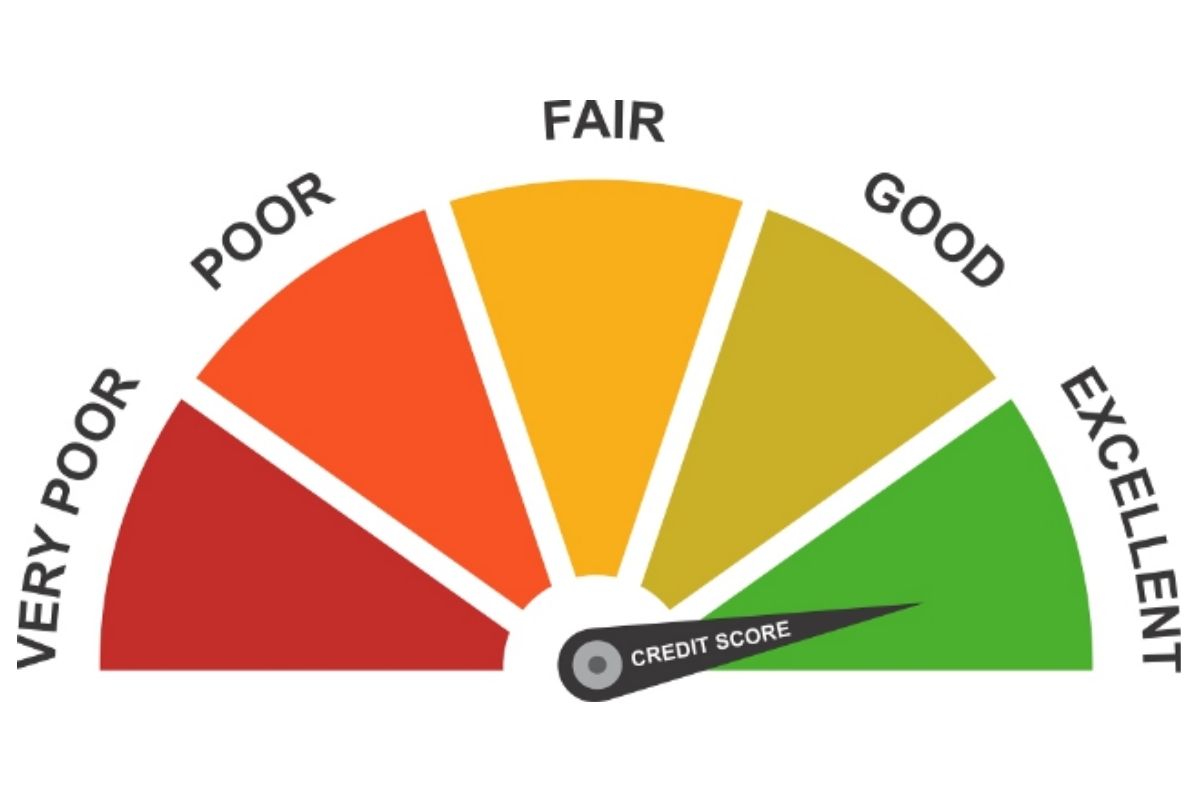

In spite of the fact that credit score ranges change contingent upon the credit scoring model, typically credit scores from 580 to 669 are viewed as reasonable; 670 to 739 are viewed as acceptable; 740 to 799 are viewed as awesome; and 800 and up are viewed as brilliant. Higher financial assessments mean you have shown capable credit conduct before, which may make expected banks and loan bosses more certain while assessing a solicitation for credit.

Banks, for the most part, observe those with credit scores of 670 and up as adequate or lower-hazard borrowers. Those with credit scores from 580 to 669 are commonly observed as “subprime borrowers,” which means they may think that it is more difficult to meet all requirements for better credit terms. Those with lower scores, usually under 580, typically fall into the “poor people” credit range and may experience issues getting credit or meeting all requirements for better loan terms.

Various loan specialists have various rules with regards to conceding credit, which may incorporate data, for example, your pay or other different components. That implies that the credit scores they acknowledge may change contingent upon that standard.

Credit scores may vary between the three significant credit departments (Equifax, Experian and TransUnion) as not all banks and loan specialists report to every one of the three. Numerous loan bosses do answer to each of the three, however you may have a record with a creditor that just reports to one, two or none by any stretch of the imagination. Also, there are various scoring models accessible, and those scoring models may contrast contingent upon the sort of credit and moneylenders’ inclination for specific rules and policies.

How To Improve Credit Score?

Here are some dependable practices to keep in mind as you build up – or keep up – capable credit practices:

Pay your bills on time, every time.

This does not simply incorporate credit cards– late or missed installments on other accounts, for example, cell phones, might be accounted for to the credit agencies, which may affect your FICO ratings (credit scores). In case you are experiencing difficulty taking care of a tab, contact the bank right away. Try not to skip installments, regardless of whether you are contesting a bill.

Pay off your debts

Do not hold off when it comes to paying your debts. Do this as quickly as you possibly can.

Keep your credit card balance well below the limit.

A higher equilibrium contrasted with your credit cutoff may affect your credit score.

Apply for credit sparingly.

Applying for various credit accounts inside a brief timeframe period may affect your credit score.

Check your credit reports regularly.

You can always request for a free duplicate of your credit report and check it to ensure that your own data is right and there is no wrong or fragmented record data. You are qualified for a free duplicate of your credit reports like clockwork from every one of the three cross country credit departments by visiting www.annualcreditreport.com. By mentioning a duplicate from one like clockwork, you can watch out for your reports all year. Keep in mind: checking your own credit report or FICO rating would not influence your credit scores.

Transunion Credit Score Range

The FICO assessment you see from TransUnion depends on the VantageScore® 3.0 model. Scores in this model reach from 300 to 850. A decent score with TransUnion and VantageScore 3.0 is somewhere in the range of 661 and 720. As your score moves through or more this reach, you can profit by the expanded opportunity and adaptability sound credit brings. A few people need to accomplish a score of 850, the most noteworthy FICO assessment conceivable. Having this “great” score may feel like a success, yet nothing explicit opens in the event that you hit that enchantment number.

Does Anyone Have An 850 Credit Score?

It’s viewed as the unicorn of the monetary world: an ideal financial assessment, the most elevated number a customer can accomplish inside a credit scoring framework. For the FICO Score, one of the most generally utilized credit scoring models, that legendary and apparently incomprehensible figure is 850. (FICO® Scores range from 300 to 850.)

Truly, Americans with an ideal 850 FICO Score do exist. Truth be told, 1.2% of all FICO Scores in the U.S. as of now remain at 850. Consider it the substitute—and maybe somewhat less charming—1 percent.

Obviously, you needn’t bother with an ideal score to get to credit at the best terms and least loan costs. By and large, scores over 700 are viewed as acceptable. Furthermore, as a commonsense issue, moneylenders don’t regularly recognize scores that are in the “excellent” scope of 800 to 850. Much of the time, a score over 760 will qualify you for the wellbeing rates. So while accomplishing a fantastic FICO assessment is an objective deserving of striving for, getting to the most noteworthy number on the scale isn’t fundamental. Additionally remember that FICO ratings are continually changing, so even those that do arrive at 850 don’t generally remain there.

What Percentage Of The Population Has A Credit Score Over 800?

Today, about 21.8% of shoppers have a FICO Score more than 800 credits, as per Experian. In 2009, just about 18.2% of the populace held a FICO rating more noteworthy than 800. The normal FICO rating in the United States hit 704 out of 2018, which is the most noteworthy it’s ever been. Specialists accept that expanded purchaser mindfulness and instruction is helping customers comprehend the significance of overseeing credit well.

Excellent Credit Score Benefits

Here are some great benefits to having a good credit score:

Low Interest Rates on Credit Cards and Loans

The interest rate is one of the costs you pay for obtaining cash and, regularly, the interest rate you get is legitimately attached to your credit score. In the event that you have a decent FICO rating, you’ll quite often fit the bill for the wellbeing rates, and you’ll pay lower account charges on Mastercard equilibriums and advances. The less cash you pay in revenue, the quicker you’ll take care of the obligation and the more cash you have for different costs.

Better Chance for Credit Card and Loan Approval

Borrowers with a helpless record normally try not to apply for another Visa or credit since they’ve been turned down beforehand. Having a fantastic FICO assessment doesn’t ensure endorsement, since banks actually consider different factors, for example, your pay and obligation. Be that as it may, a decent FICO assessment expands your odds of being affirmed for new credit. At the end of the day, you can apply for an advance or Visa with certainty.

More Negotiating Power

A decent FICO assessment gives you influence to arrange a lower financing cost on a Mastercard or another advance. In the event that you need additionally dealing power, you can exploit other alluring offers that you’ve gotten from different organizations dependent on your FICO rating. Be that as it may, on the off chance that you have a low FICO rating, lenders are probably not going to move on advance standing, and you won’t have other credit offers or alternatives.

Get Approved for Higher Limits

Your obtaining limit depends on your pay and your FICO assessment. One of the advantages of having a decent financial assessment is that banks are eager to let you acquire more cash since you’ve exhibited that you take care of what you get on schedule. You may at present get endorsed for certain advances with a terrible FICO assessment, yet the sum will be more restricted.

Easier Approval for Rental Houses and Apartments

More landowners are utilizing FICO assessments as a component of their occupant screening measure. A terrible FICO rating, particularly if it’s brought about by a past removal or exceptional rental equilibrium, can seriously harm your odds of getting into a loft. A decent FICO assessment spares you the time and bother of finding a property manager that will affirm tenants with harmed credit.

Better Car Insurance Rates

Add auto insurers to the rundown of organizations that will utilize a terrible FICO assessment against you. Insurance agencies use data from your credit report and protection history to build up your protection hazard score, so they regularly punish individuals who have low FICO ratings with higher protection charges. With a decent financial assessment, you’ll commonly pay less for protection than comparable candidates with lower FICO ratings.

Get a Cell Phone on Contract With No Security Deposit

Another downside of having a terrible financial assessment is that wireless specialist organizations may not give you an agreement. All things being equal, you’ll need to pick one of those pay-more only as costs arise plans that have more costly telephones. At any rate, you may need to pay extra on your agreement until you’ve set up yourself with the supplier. Individuals with great credit try not to pay a security store and may get a limited price tag on the most recent telephones by marking a contract.

Avoid Security Deposits on Utilities

These security deposits are at times $100 to $200 and an immense burden when you’re moving. You may not be intending to move soon, yet a cataclysmic event or an unanticipated condition could change your arrangements. A decent financial assessment implies you won’t need to pay a security store when you set up utility assistance in your name or move administration to another area.

Bragging Rights

Due to all the advantages, a decent financial assessment is something to be glad for, particularly on the off chance that you’ve needed to endeavor to assume your acknowledgment score from awful to great. Furthermore, in the event that you’ve never needed to encounter an awful FICO assessment, continue taking the necessary steps to keep up your great score. It just takes a couple of missed installments to begin getting off track.

What is a good FICO score?

A good FICO score lies between 670 and 739, according to the company’s website. FICO says scores between 580 and 669 are considered “fair” and those between 740 and 799 are considered “very good.” Anything above 800 is considered “exceptional.”

According to FICO, the average credit score in 2021 was 716, which falls in the good range.

FICO comes from Fair Isaac Corp., the company that first developed a credit scoring system. It uses data about consumers from the three major credit reporting bureaus: TransUnion, Equifax and Experian.

FICO scores typically express a consumer’s creditworthiness as a number between 300 and 850.

What is a good VantageScore?

FICO’s competitor, VantageScore produces a similar score using the same credit report data from the three bureaus. (NerdWallet offers you a free credit score using VantageScore and your TransUnion credit report.)

A good VantageScore lies between 661 and 780, which the company calls a “prime” credit tier. VantageScores above 780 are considered “superprime” while those between 601 and 660 are “near prime.” VantageScores below 600 are considered “subprime.”

Why Having a Good Credit Score Is Important

There are a lot of reasons why having a good credit score is important. For one, it can help you get approved for loans and lines of credit. A good credit score means you’re a low-risk borrower, which makes lenders more likely to approve your loan or line of credit application.

A good credit score can also help you get a lower interest rate on your loan. That’s because lenders view borrowers with good credit scores as less of a risk, and so they’re willing to offer lower interest rates to these borrowers. This can save you a lot of money over the life of your loan, since you’ll be paying less in interest.

Finally, a good credit score can also help you get a better insurance rate. Many insurers use credit scores to help determine premiums, so having a good credit score could lead to a lower insurance rate.

All of these reasons show why it’s so important to have a good credit score. If you’re not sure what your credit score is, you can check it for free on AnnualCreditReport.com. And if you find that your credit score isn’t as high as you’d like, there are steps you can take to improve it.

Tips for Boosting Your Credit Score

To build a good credit score, practice these habits consistently:

- Pay Bills on Time

Payment history affects your score the most. Late or missed payments can significantly damage your score and stay on your report for up to seven years. - Maintain Low Credit Utilization

Keep your credit card balances well below your limits. Aim for credit utilization under 30%; lower is better. High utilization can harm your score, but reducing balances will help. You can also lower utilization by increasing your credit limit or becoming an authorized user on a lightly used card with a large limit. - Keep Credit Accounts Open

Unless there’s a compelling reason like high fees or poor service, keep your credit accounts open. Older accounts help your average age of accounts, which positively impacts your score. Closing an account decreases your overall credit limit, increasing your credit utilization. - Limit Credit Applications

Avoid making several credit applications in a short period. Each credit check for new credit can cause a small, temporary dip in your score. Multiple checks in a short time can add up, so research credit cards before applying. - Monitor Your Credit Reports

Regularly check your credit reports and dispute any incorrect or outdated information. Most negative information falls off after seven years.

By following these tips, you can build and maintain a strong credit score.

Learn More About Credit Scores

What Is the Average Credit Score in the U.S.?

The average credit score in the United States is 699. This number has been steadily rising over the past few years, and it’s now at its highest point since Credit Sesame began tracking scores in 2010.

What Affects Your Credit Scores?

There are a lot of different things that can affect your credit scores. Payment history is one of the biggest factors, so if you have any late payments or collections, it will hurt your scores.

Credit utilization is another big factor. This is the percentage of your credit limit that you’re using. So, if you have a high credit utilization, it will hurt your scores.

The types of credit you have can also affect your scores. It’s generally better to have a mix of different types of credit, like revolving credit and installment loans. This shows lenders that you’re able to handle different types of credit responsibly.

What Are the Different Credit Scoring Ranges?

Credit scores range from 300 to 850. The higher your score, the better. Here’s a breakdown of what each range means:

300-579: This is considered a “poor” credit score. If your score is in this range, it’s going to be difficult to get approved for loans and credit cards.

580-669: This is considered a “fair” credit score. If your score is in this range, you may be able to get approved for some loans and credit cards, but you’re likely to have a higher interest rate.

670-739: This is considered a “good” credit score. If your score is in this range, you’re likely to get approved for most loans and credit cards. You’ll also probably get a lower interest rate.

740-799: This is considered an “excellent” credit score. If your score is in this range, you’re likely to get approved for all loans and credit cards. You’ll also probably get a lower interest rate.

What Is a Bad Credit Score?

A bad credit score is generally any score below 630. If your score is in this range, you’re going to have a hard time getting approved for loans and credit cards. And if you are approved, you’re likely to get stuck with high interest rates and fees.

What Makes a Good Credit Score?

A good credit score is generally anything above 700. If your score is in this range, you’re going to have an easier time getting approved for loans and credit cards. And if you are approved, you’re likely to get more favorable terms, like low interest rates and fees.

Conclusion

You don’t need a perfect financial assessment to reach your goals. You can buy a home, return to school, or open a credit card without an 850-point score. However, you can achieve a perfect score with years of proper credit management. If you have a 750-point score, you’re still in the “very good” credit club. However, you might want to improve your score if you seek the best offers available.

If you’re striving for a perfect FICO® Score, consider these tips as you work toward your goal. Remember, having multiple credit cards or lines of credit isn’t bad unless you mismanage your debt. Open new accounts when needed and manage your debt and payments responsibly. Make payments on time and keep your debt levels low. Avoid any delinquent accounts.

If you’re building your credit score, regularly check your credit reports and scores. Monitor what’s in your record and how it affects your score.