What Is The Best Way To Find Affordable Health Insurance?

Wondering about the best way to find affordable health insurance? There are many health insurance policies available in the market, but selecting the best one that meets one’s needs may not be easy. Read more to familiarize yourself with what to consider while choosing one.

Navigating the world of health insurance can be surprising, but with the right strategies, you can find a low-cost plan that meets your needs. Understanding the services, costs, and attributes of care is essential. And the good news is this season brings positive changes for those seeking health coverage outside of work. Thanks to the Biden administration, the Affordable Care Act has been updated with extended enrollment periods, improved assistance, and subsidies for ACA marketplace plans, making it even easier to find the right coverage for you.

The world of employer-based health insurance options can feel like a puzzle. Trying to juggle your health needs, finances, and all the insurance terminology can be overwhelming. Whether diving into security for the first time, upgrading your cover, or exploring different alternatives, our guide is here to make things easier. Instead of focusing only on the monthly cost, take a broad look at your options. Remember to consider allowance and copays for more comprehensive coverage.

And don’t worry about getting lost in the sea of slang; our glossary will give you the tools you need to make informed decisions. We’ve got your back. We’ve got your back; if you need clarification on which plan is right for you, we’ve got your back. From preventive care to prescriptions, harmonize premiums, deductibles, and anticipated medical necessities. Need help with low premiums and out-of-pocket maximums? We demystify the trade-offs, guiding your informed selection. Evaluate metal tiers, location, and income-based plans to secure an optimal match. Our assessment of 14 major insurers transcends premiums.

Customer contentment, plan advantages, and attainable discounts inform our recommendations. Unearth the most economical options tailored to your specific needs. Let our blog illuminate the path to obtaining affordable health insurance. Find clarity, steering you toward financial security and premium healthcare coverage.

Best health insurance plans

When people look for low-cost health insurance, the first thing that comes to mind is the price. Consumers have a broad perception that low-cost health plans should not be expensive. And that the lowest-cost health plan on the market should be their goal. This strategy, however, is compelling. Paying for a low-cost health insurance plan but not receiving the appropriate level of coverage can result in a good use of money.

With the passage of the Affordable Care Act, more people can afford health insurance. At the very least, this is considered the goal of healthcare reforms. However, many people still need clarification as to how things will operate.

Consumers must do a few things to obtain affordable health insurance policies. The first is to be aware of the possibilities available in one’s particular state of residency. Consumers may be eligible for a variety of state and federal government-run programs. However, the next step is to familiarize yourself with the terms and conditions of each program and the eligibility requirements for each.

Furthermore, customers should be aware of their rights following the adoption of healthcare reforms, as they may qualify for certain programs or be permitted to purchase a specific health insurance plan within a few days if customers follow these procedures. There is no reason why they cannot choose an affordable health plan that meets their medical needs.

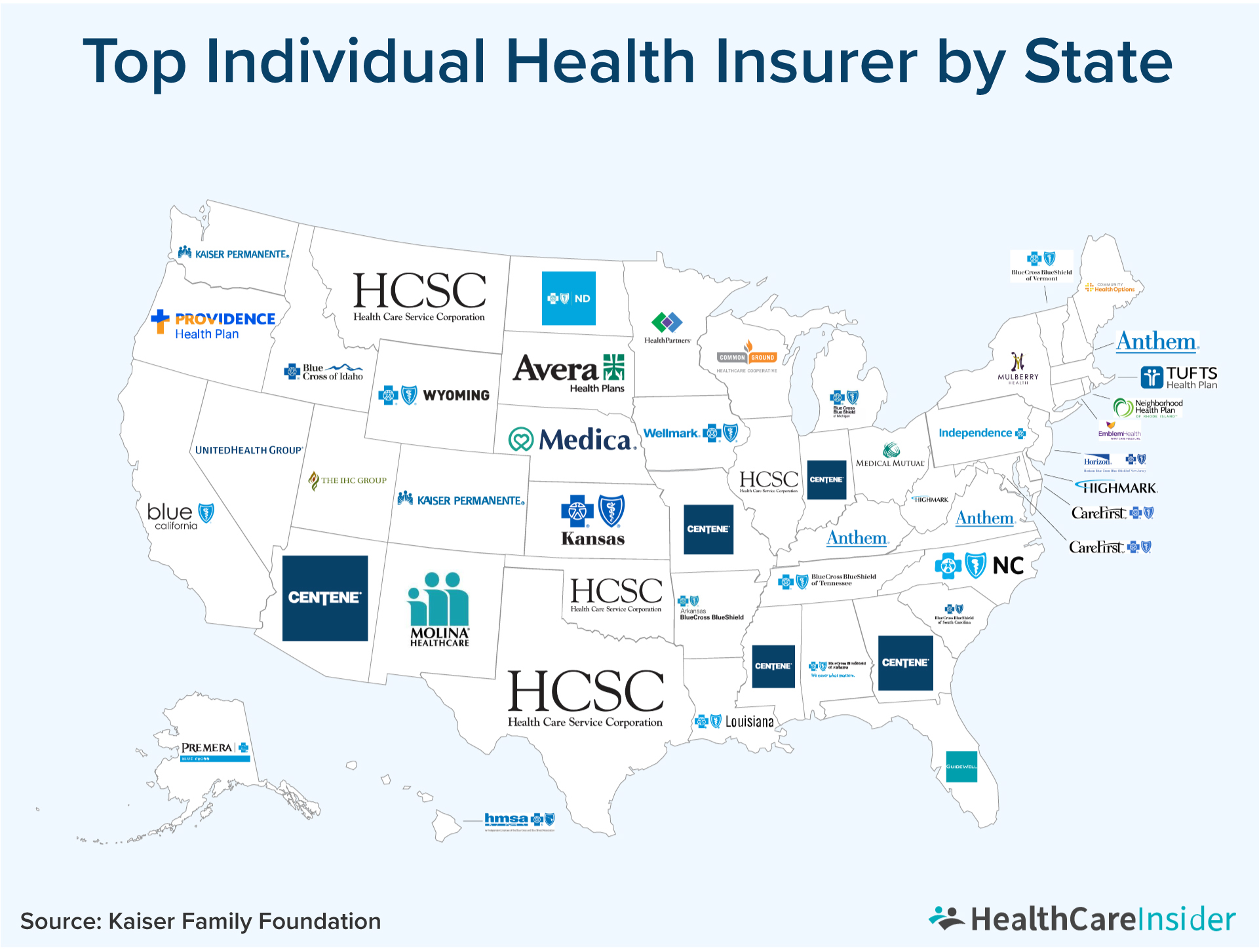

State-wise affordable health insurance plans

California: Accessible health coverage

California offers an array of state-administered, cost-effective health insurance plans. With three viable options overseen by the state government, eligible individuals can reap the benefits.

- Major risk medical insurance program (MRMIP): This program extends valuable health benefits to California residents with pre-existing medical conditions. Eligible consumers can inquire about their qualifications and avail the benefits.

- Healthy Families program: Geared toward children whose parents earn too much for government aid. This initiative provides affordable health, dental, and vision coverage. Managed by MRMIP, it ensures comprehensive care for youngsters.

- Access for Infants and Mothers Program (AIM): AIM caters to low-income pregnant women, offering prenatal and preventative care. Governed by a dedicated board, it assembles a comprehensive benefits package, including inpatient and outpatient services.

Florida: Tailored solutions

Exploring affordable health insurance choices in Florida involves these options:

- COBRA continuation coverage is a safety net for those who’ve lost employer-based group insurance.

- The covered Florida limited health benefit plan may be suitable if you’ve been uninsured for six months.

- Floridians with modest incomes can explore the Florida Medicaid program, which offers coverage for pregnant women, children, the medically needy, the elderly, and people with disabilities.

- The Florida KidCare program assists uninsured or underinsured children under 19 who aren’t eligible for Medicaid.

Virginia: Affordable assurance

Navigating health insurance options in Virginia entails these considerations:

- Individuals facing loss of employer-sponsored group health insurance can turn to COBRA or state-sponsored continuation coverage.

- Anthem Blue Cross Blue Shield or CareFirst Blue Cross Blue Shield Individual health plans for Virginia residents.

- The Virginia Medicaid program assists those with low or modest household incomes, aiding pregnant women, families with children, the elderly, and people with disabilities.

- FAMIS (Family Access to Medical Insurance Security) supports uninsured Virginian children under 18.

Texas: Rights and coverage

Searching for affordable health insurance in Texas? Familiarize yourself with your rights and explore these avenues:

- Texans with group insurance cannot be denied coverage or subjected to excessive charges due to health conditions. It cannot exclude pre-existing diseases from group health insurance.

- Insurance companies prohibit terminating coverage for Texans who fall ill. COBRA or state continuation coverage is accessible for HIPAA-eligible Texans.

- The Texas Medicaid program provides free or reduced health coverage for those with low or modest incomes, helping pregnant women and relatives, the elderly, and people with disabilities. A breast or uterine cancer diagnosis may also qualify for Medicaid.

- The Texas Children’s Health Insurance Program (CHIP) provides supported coverage for assured children. Healthcare reforms enable children in Texas to remain on their parent’s policy until they turn 26.

- The Texas Breast and Cervical Cancer Control Program extends free cancer coverings for limiting residents, offering Medicaid care upon diagnosis.

Navigating affordable health insurance involves exploring state-specific opportunities. Equipping yourself with information is critical to securing the right health plan for your needs.

Best Affordable Health Insurance Companies

Certain companies rise above the rest when seeking health insurance that seamlessly combines quality and affordability. In the ever-evolving realm of healthcare, Aetna, Oscar, Kaiser Permanente, and Molina Healthcare have garnered recognition for their exceptional offerings. Let’s delve into the distinctive features of that set. These companies apart and the advantages and disadvantages associated with each:

Aetna: Unleashing affordability through tax credits

Pros

- Aetna offers the potential for a $0 premium through premium tax credits.

- It provides access to $0 same-day CVS MinuteClinic

- Additionally, it introduces ultra-low-cost bronze plans for 2023.

Cons

- However, it features high deductibles on select low-cost plans.

Why did we choose Aetna?

Aetna distinguishes itself by prioritizing health insurance plans that qualify for maximum premium tax credits. It translates to the possibility of having a $0 premium if you meet the necessary criteria. Furthermore, Aetna’s partnership with CVS MinuteClinics ensures convenient access to urgent care. The addition of low-premium bronze plans further enhances Aetna’s appeal.

Oscar: Affordable plans with enhanced value

Pros

- Oscar offers budget-friendly plans across various metal tiers

- While also facilitating $0 virtual urgent care through the Oscar app.

- Motivates healthy living by rewarding you for reaching step goals.

Cons

- Despite its strengths, Oscar receives relatively lower ratings from NCQA and CMS.

- Additionally, its operations are limited, available in just 21 states.

Why did we choose Oscar?

Oscar approaches health insurance innovatively, leveraging technology to augment its value proposition. However, offering a range of cost-effective plans spanning diverse metal levels, Oscar is ideal for those who prioritize affordability without compromising coverage. Additional perks such as $0 virtual urgent care and incentives for maintaining an active lifestyle contribute to its allure.

Kaiser Permanente: Elevating the customer experience

Pros

- Attains high ratings for customer satisfaction from multiple sources.

- Kaiser Permanente provides competitively priced premiums

- In addition, it proudly boasts 5-star ratings from healthcare.gov and 3 stars from the NCQA.

Cons

- It may entail higher deductibles.

- It operates within limited boundaries and is available in eight states and the District of Columbia.

Why do we choose Kaiser Permanente?

Kaiser Permanente excels in delivering an exceptional customer experience. With its impressive customer satisfaction ratings and competitive premium rates. Kaiser is an attractive option for those who value premium service. However, its availability remains restricted to specific states.

Molina Healthcare: Linking affordability and comprehensive coverage

Pros

- Molina Healthcare offers bronze plans with notably lower deductibles, providing greater affordability for essential coverage.

- Additionally, Molina extends its coverage to encompass bronze, silver, and gold plan tiers, ensuring a comprehensive range of options for customers.

Cons

- However, it’s worth noting that Molina Healthcare receives a 2-star rating from Healthcare.gov, indicating room for improvement in certain areas.

- Primarily offers HMO plans, limiting provider choices.

Why we chose Molina Healthcare?

Molina Healthcare shines in the realm of seamlessly combining affordability and comprehensive coverage. With bronze plans featuring reduced deductibles compared to competitors. Molina becomes a practical choice for those seeking coverage beyond preventive care. However, it’s crucial to consider the 2-star rating from Healthcare.gov and the HMO plan structure when making your decision.

As you contemplate these leading affordable health insurance providers, remember that determining the “best” fit depends on your unique needs, preferences, and geographical location. Therefore, striking a balance between premiums, deductibles, provider networks, and supplementary benefits will guide you toward the most suitable option for your healthcare journey. Ultimately, making an informed choice empowers you to achieve financial stability and comprehensive coverage.

Key considerations when seeking affordable healthcare

When selecting an affordable health insurance plan, there may be more effective strategies than focusing solely on the lowest cost. It must consider numerous essential factors to ensure a comprehensive and budget-friendly decision.

Assess your health care needs

Take into account both your health requirements and those of your family. Opting for the cheapest plan without aligning it with your health needs could result in higher expenses later. Hence, pause to assess your monthly premiums, investigate different mental forms if ACA plans are on your radar, and consider the advantages of having a Health Savings Account (HSA) or Flexible Spending Account (FSA). Additionally, factor in potential out-of-pocket costs to gain a more precise knowledge of the overall accessibility of the plan.

Grasp the benefit of design

The both insurance plan’s benefit design is pivotal in determining its usability. Various methods, such as Health Maintenance Organization (HMO) and Preferred Provider Organization (PPO), come with varying levels of flexibility and coverage. While HMOs are more budget-friendly, they impose more restrictions on provider options. PPOs offer heightened flexibility but may entail higher associated costs. Striking a harmonious balance between affordability and flexibility becomes crucial.

Explore the provider network

Provider networks play a pivotal role in health insurance plans. These networks outline medical professionals and hospitals deemed “in-network.” Opting for in-network providers generally incurs lower costs compared to out-of-network choices. However, specific plans, mainly HMOs, may only cover out-of-network emergency care. Before finalizing a project, ensure that your preferred healthcare providers are part of its network.

Examine the cost structure

While premiums constitute a visible component of health insurance expenses, delving deeper and analyzing other cost elements is essential—the deductible, coinsurance, and out-of-pocket maximum influence a plan’s affordability. Strive to balance monthly premium payments and potential expenses you might incur when seeking medical attention.

Evaluate prescription drug coverage

If you rely on prescription medications, pay keen attention to a plan’s prescription drug coverage. Understand how much the health plan will contribute to your prescription drug expenses. Therefore, robust prescription drug coverage can significantly impact a health insurance plan’s affordability, particularly for individuals with ongoing medical requirements.

Pursue additional benefits

Modern health insurance plans often encompass supplementary benefits and features beyond traditional coverage. Seek out programs offering health-related applications, round-the-clock hotlines for medical guidance, and the convenience of telehealth visits. These additional services can elevate the overall value of a health insurance plan and contribute to a more comprehensive healthcare experience.

Comprehending affordable health insurance: Key insights to embrace

Navigating the realm of cheap health insurance involves more than finding the lowest price. It’s essential to grasp the nuances of health insurance terms and options to make an informed choice. Here’s a comprehensive overview to guide your quest for affordable health insurance.

Understanding the financial landscape

The financial aspects merit careful consideration when securing cheap health insurance. However, the monthly premium often takes the spotlight, but multiple factors contribute to the overall cost. Variables such as the deductible amount, geographical location, chosen plan type, coverage scope, age, smoking status, household size, and income collectively influence the premium.

Take a comprehensive view of the expenses, including premiums, deductibles, and coinsurance, to clearly show each plan’s affordability. Remember that Health Maintenance Organization (HMO) plans tend to have lower premiums but may restrict your choice of healthcare providers. In contrast, Preferred Provider Organization (PPO) plans offer greater flexibility at a potentially higher cost.

Unpacking the metal categories

The Affordable Care Act (ACA) classifies health insurance plans into four “metal” classes, reflecting the allocation of costs between you and the insurance provider. Each class offers a distinct balance between premiums and out-of-pocket costs:

- Bronze: Characterized by the lowest monthly premiums, bronze plans entail higher deductibles. These plans suit individuals seeking coverage for unforeseen emergencies. Your health insurance covers 60% of costs, while you bear 40%.

- Silver: Slightly higher premiums accompany silver plans but offer reduced costs when you require medical attention. These plans encompass a 70-30 cost-sharing split between your insurance and yourself. If eligible, you may qualify for cost-sharing subsidies.

- Gold: Opt for gold plans if regular medical visits are part of your routine. These plans feature higher monthly premiums but lower point-of-care expenses. The cost distribution is 80% by the insurance and 20% by you.

- Platinum: With the highest monthly premiums, Platinum plans assure extensive coverage with minimal point-of-care expenses. Platinum plans ensure comprehensive coverage with point-of-care minimal expenditures. They are suitable for individuals requiring frequent medical care.

Harnessing premium tax credits

Whether your preference leans toward a bronze, silver, gold, or platinum plan, leveraging premium tax credits can significantly enhance affordability. These credits work to reduce monthly health insurance payments, rendering coverage more accessible. So, eligibility criteria hinge on household income, with those at or below 400% of the federal poverty level qualifying for these credits. Additionally, specific silver plans may offer cost-sharing subsidies to alleviate out-of-pocket expenses.

Navigating health savings accounts (HSAs) and flexible spending accounts (FSAs)

Distinguishing between HSAs and FSAs is pivotal when searching for the most cost-effective health insurance plan. HSAs accompany high-deductible health plans (HDHPs) and cater to individuals with deductibles meeting specific criteria. These accounts empower you to allocate pre-tax funds towards qualified medical expenses, reducing overall healthcare costs. Unlike FSAs, HSAs are versatile and can persist even after retirement.

In contrast, FSAs are often offered by employers alongside health insurance plans. These accounts allow you to allocate pre-tax earnings towards medical expenses, but the funds usually don’t roll over to the following year. To make an informed choice between FSA and HSA, consider their key differences:

FSA |

HSA |

|

| HDHP | Not necessary | Required Limit |

| Limit | Employer-set, up to $2,800 | Up to $3,850 for single, $7,750 family |

| Rollover | Typically not | Yes |

| Portability | Yes (changing employers) | No |

Out-of-network coverage

Caution and Choice: Seeking in-network providers is generally more affordable than opting for out-of-network care. Visiting an out-of-network provider could lead to substantial additional costs. To ensure affordability, prioritize plans that accommodate your preferred care providers within their network. Alternatively, explore programs offering flexible out-of-network coverage without exorbitant expenses.

Uncover the out-of-pocket maximum.

The out-of-pocket maximum represents the highest annual expenditure for healthcare services. In-network deductible payments, copays, and coinsurance contribute to this cap. Premiums, charges for uncovered services, and out-of-network costs don’t factor in. Upon reaching this maximum, insurance covers 100% of the expenses for the remainder of the year. Carefully evaluating the out-of-pocket maximum can guide you towards the most affordable health care plan aligned with your needs.

Selecting the Right Affordable Health Insurance Provider

As you compare health insurance quotes to identify the optimal affordable health insurance solution, consider the following factors to make an informed decision:

- Comprehensive health plan assessment: Take a holistic approach by evaluating the complete health plan cost. Examine various elements such as the monthly premium, deductible, coinsurance, copayments, and the out-of-pocket maximum. This comprehensive analysis provides a clear understanding of the overall financial commitment.

- Variety of plan options: When seeking the most economical health plan benefit structure, explore alternatives such as a Health Maintenance Organization (HMO) or an Exclusive Provider Organization (EPO) plan. These options require adhering to the designated provider network, resulting in lower premiums than a Preferred Provider Organization (PPO) plan. While a PPO offers enhanced flexibility, it often comes with a higher price point.

- Projected healthcare needs: Tailor your selection to your anticipated healthcare requirements. Opt for a high-deductible health plan if you expect minimal healthcare needs. Conversely, if you foresee frequent medical attention, consider a project with a slightly higher premium but a lower deductible—this approach could lead to significant savings over the year.

- Provider compatibility: Place priority on confirming that your healthcare providers accept your chosen health insurance plan before finalizing your decision. Directly consult your providers to ensure they are affiliated with the specific insurance plan you are considering. Exercise caution with online provider directories provided by insurance companies, as they can be inaccurate or outdated.

- Exploring all avenues: Investigate the chance of joining another individual’s health plan, as it may offer a more cost-effective substitute to buying your insurance. Assess all available health insurance options a spouse or parent provides to ensure you make a well-informed choice that arranges with your budget and health care needs.

How to find cheap health insurance easily?

Almost everyone requires health insurance, and they need a program that matches the demands of their family, covers the services they require, and works within their budget. While some customers think they should be able to select an insurance company with lower prices than the competition, this is various.

Insurance firms usually have a type of goods to choose from. They offer a wide range of insurance options. Some of the affordable plans are essential, no-frills options. To select a cheap health insurance carrier that meets your personal needs, follow these three steps:

Determine the size of the insurance firm. Companies have more negotiating leverage when collecting fees for working with doctors and hospitals. They can negotiate cheaper rates for the services you use so that they offer you lower insurance premiums. On the other hand, smaller insurance businesses have different bargaining strengths and must frequently pay more for the same services. As a result, you will have to spend more.

Compare plans and get instant quotes. You can acquire rapid prices on insurance policies from several businesses over the Internet. Quote engines are tools on some websites that allow you to receive and compare numerous quotes. It is as easy as entering your zip code and selecting a few options.

You will get a collection of quotes in less than 10 seconds. You can save money on needless services and acquire a much more reasonable health insurance plan that matches your needs by comparing plans and picking ones that only provide the services you need and desire. Men, for example, do not require maternity coverage.

Search for the company. Make sure the affordable health insurance business you choose has a solid reputation before you choose and pay for a health insurance plan. You can see how current customers have rated the firm and the project. Take a look around for some input. You want to know that your low-cost health insurance provider is credible.

How do you save money with insurance coverage?

There are things you can do to help save even more money on medical bills, in addition to saving money on insurance premiums. Here are some tips:

- Get quotes from several companies to compare specific services and procedure rates. For the same treatment, some providers charge significantly less than other facilities.

- Only go to the ER if it is an absolute emergency. Otherwise, visit a walk-in clinic or schedule an appointment with your doctor.

- Before visiting a doctor, try home cures for common diseases. First, see if they work or not.

- Do not have X-rays taken every time you go to the dentist. X-rays are only required every one or two years.

- For prescription drugs, use a mail-order service.

- If a generic prescription drug is available, request it instead of the name brand.

- Choose a health insurance plan with a larger deductible. Your rates will be lower, and you will be ahead financially at the end of the year if you do not use health insurance services frequently.

- Pay premiums every year. You can gain savings compared to monthly payments, including a service fee.

- When you have the opportunity, visit a local free clinic.

Finding a low-cost health insurance provider is one step toward ensuring your family’s medical needs are addressed within your budget. When combined with these tips, you will be able to manage your healthcare expenses better.

Affordable health insurance according to one’s needs

Everyone is looking for cheap health insurance these days. With the rising costs of everything, including gasoline, managing a household budget is getting tougher. Health insurance is a significant expense that many households struggle to afford.

Finding ways to save on health insurance can free up your income and provide more breathing room in your monthly budget. Given stagnant wages, reducing costs wherever possible is essential. Health insurance, being one of the more expensive necessities, offers a prime opportunity for savings. Protecting your family in case of an accident or illness is crucial, despite the soaring costs of medical treatment and insurance premiums.

Securing low-cost health insurance is critical. Imagine the possibilities if you could reduce your health insurance rates—more money for other needs and wants. Finding affordable health insurance that fits your budget and provides adequate coverage is easier than you think.

No family can afford to be without health insurance. A serious illness can mean the difference between financial stability and catastrophe. You need the best service while keeping costs low. Start by comparison shopping. Many companies offer low-cost health insurance, but not all plans are equal.

First, understand the types of coverage you need, choose your deductible, and set a suitable cap amount. The deductible is the amount you pay before the insurance starts to cover expenses. Higher deductibles mean lower premiums. Review your past health expenses. If you’ve had minor issues and few doctor visits, a higher deductible might be best.

If you anticipate significant medical bills, opt for a lower deductible even if it means higher premiums. This ensures your insurance covers more costs. Affordable health care insurance is available, but you must research and evaluate your needs. Many find that online quotes offer the best coverage and plans for their money.

FAQs

How much does health insurance cost?

Health insurance costs vary depending on location, age, plan choice, and smoking status. Bronze plans on the Health Insurance Marketplace are known for being the most affordable, with prices influenced by your circumstances.

What is the premium tax credit?

The premium tax credit, fixed by the Affordable Care Act (ACA), aims to make Marketplace health insurance premiums more available. Eligibility requires a modified adjusted gross income (AGI) between 100% and 400% of the federal poverty level (FPL), with brief changes due to the American Rescue Plan Act of 2021.

What does a deductible mean in health insurance?

A deductible is the amount you must pay out of pocket before your insurance covers expenses. This yearly payment contains copays for doctor visits, medicine drugs, and franchising, with an out-of-pocket maximum defined as the limit before insurance covers 100% of costs.

What is a high-deductible health plan (HDHP)?

An HDHP offers low monthly premiums in exchange for a higher deductible. The IRS defines an HDHP with an allowable of $1,500 for individuals and $3,000 for families in 2023. These plans often come with a health savings account (HSA) to save money for skilled healthcare costs.

Which health insurance type is most affordable?

Oscar is a recommended value plan, while Molina Healthcare offers the most cost-effective bronze plans. Your specific coverage needs and personal circumstances will determine the actual cost of your health insurance plan.

What qualifies as a life event for special enrollment?

Life events like changing residence, having a new baby, getting married, or losing health coverage can make you eligible for special enrollment in the Health Insurance Marketplace. Some of these events may also trigger a particular enrollment period for your employer’s health plan.

Can I buy affordable health insurance anytime?

Typically, you can only buy or change health insurance plans during the annual open enrollment period unless you experience a qualifying life event. Open enrollment for ACA marketplace plans is usually from Nov. 1 to Dec. 15, though specific dates may vary by state.

What life events qualify for special enrollment?

Life events such as losing health insurance, marriage, divorce, having a baby, experiencing a family death, or moving to a different ZIP code can qualify you for special enrollment outside of the regular open enrollment period.

Should I consider a health insurance broker?

Health insurance brokers can provide valuable assistance if you’re self-employed or lack employer-sponsored insurance. They offer personalized plan recommendations and are licensed by the state. Brokers are compensated through commissions from major insurance companies, offering a reliable way to find the best affordable health insurance plan for your needs.

Conclusion

Health insurance is critical, especially in today’s world. Finding affordable health insurance can be tricky, but with some research, you can locate a plan that suits your needs and budget. Start by determining the coverage you require. If you’re younger, a nonsmoker, and don’t have severe pre-existing conditions, your needs will differ from someone older, with a family, or with pre-existing medical issues.

Individual health insurance tends to be more expensive than group health insurance. However, if you’re self-employed, you might find groups of other self-employed individuals who have formed clubs to secure group insurance rates. Finding such a group requires some effort, but it’s worth it for the potential savings. If you can’t find a group rate, you’ll need to look into individual insurance policies.

One of the best ways to find affordable health insurance is by shopping around for quotes, which is easier than ever thanks to the Internet. Understanding the various types of insurance available is also crucial. Generally, you need to see a doctor first, who will refer you to a specialist if necessary. When you follow this process, your insurance will cover the costs as outlined in your policy.

If you visit a specialist without a referral, your insurance might not cover the expenses. Finding the best affordable health insurance can be challenging, but with careful consideration of all the information, you can make an informed decision. Remember, everyone’s needs vary, so choose a plan that fits your specific requirements.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}