What Is The Highest Credit Score You Can Have?

A FICO credit score rating is important to determine the creditworthiness of a borrower.

A FICO analysis in April 2019 shows that 1.6% of Americans have excellent FICO ratings. The most effective rates and conditions on various financial products, including credit cards, mortgages, student loans, auto loans, and personal loans, are often available to consumers who reach this height. You must aim for a credit score of 850 if you want to have flawless credit. For the most popular iterations of both credit scoring algorithms, that is the highest FICO score and VantageScore that is currently accessible.

Although it can seem complicated, Forbes Advisor is available to assist. We’ll go over the actions you can take to achieve the best credit score. There are, in fact, people in America with FICO scores of 850. Currently, 1.6% of all FICO Scores are above 850. It could seem alarming, given that 11% of Americans think Bigfoot is genuine. However, a perfect score is unnecessary to get the best conditions and lowest interest rates on a loan. In most circumstances, a score of 700 or more is considered good.

Additionally, the “exceptional” range of 800 to 850 usually has no impact on lenders. You often qualify for the best rate with a score of at least 760.

A credit score is a critical metric when it comes to deciding whether you are a responsible credit user or not. Whether you’re applying for a personal loan, a mortgage, or an insurance plan, the lender or the lending company will first ask your credit score. There are means to enhance your credit score and consider what a high credit score is. And there are important reasons why your credit score always needs to be excellent. Continue reading to know.

Credit Scores

A credit score ranges from 300-850, depicting how well and worthy a person is of a loan. The greater the credit score, the better your odds of scoring a bigger loan- and that, too, very quickly.

A credit score is based on various indicators: number of open accounts, total debt levels, repayment history, and other factors. Credit scores fluctuate with time; what is a bad credit score? They are not a standard number that stays with you until time ends. If you’re responsible for paying your dues on time, your credit score will likely increase, and vice versa.

What is the highest Credit Score you can have?

The topic of who has the best credit score typically comes to mind. The majority of credit scoring systems have a scale with a 300-850 range. However, some credit scoring models, including those utilized by some institutions, exceed 900 or 950.

What is the highest credit score? So the highest score that you can go up to is 850. However, you don’t need to exhaust yourself to reach that 850. Any score in the late 700s to early 800s is a significant, perfect credit score number. You are fine with the procedure with that loan’s highest credit score.

It is the average breakdown to be mindful of:

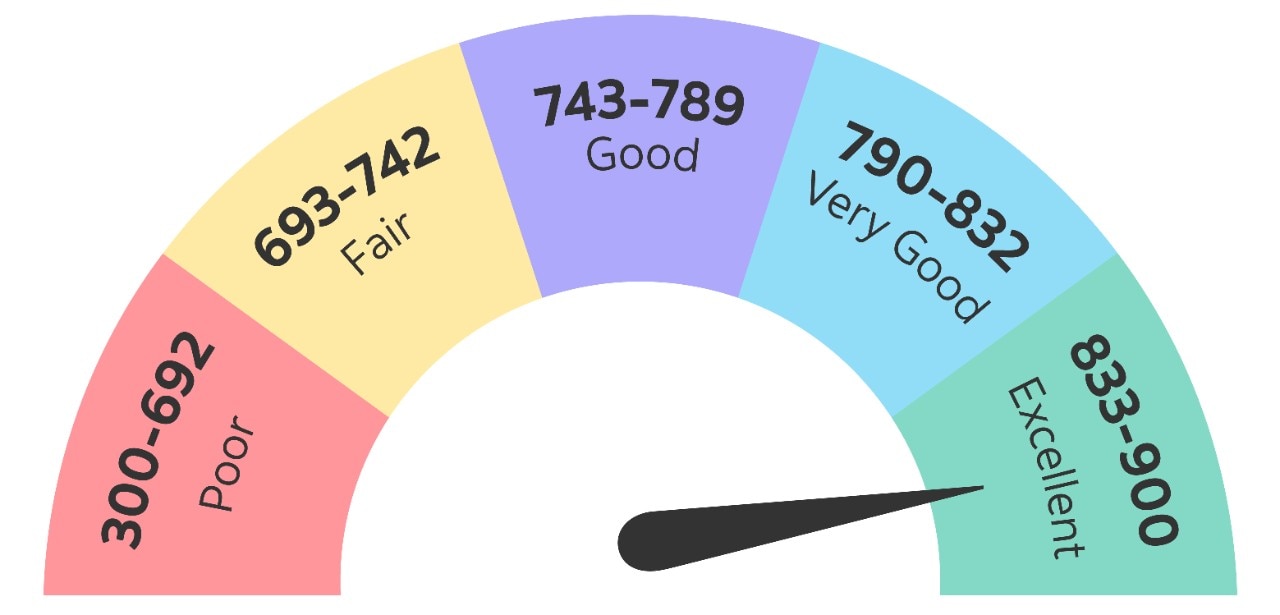

- Excellent: 800 to 850

- Very Good: 740 to 799

- Sound: 670 to 739

- Fair: 580 to 669

- Poor: 300 to 579

What is the lowest Credit Score?

According to the FICO credit score range, a person’s lowest credit score is 300. But luckily, most people don’t have a score as low as this.

But a score below 540 is considered bad credit. Thus, many people are denied loans and credits based on this FICO score. Moreover, the average score that people have in the US is 704.

Is an 850 Credit Score Possible? Here’s How to Achieve It!

Many wonder if an 850 credit score is achievable. While it might seem like a myth, 1.2% of Americans hold this perfect FICO score! So, yes—it is possible.

But is it necessary to reach 850? Not really. A credit score of 740 or higher is excellent and will still qualify you for lower insurance premiums and better financial opportunities.

How to Achieve a Perfect 850 Credit Score

- Manage Utilization: Pay off your balance before the statement closes to lower your credit utilization. This helps maintain better control over your spending.

- Budget Wisely: Create a budget to track unnecessary expenses. Reducing these will lower your need for credit.

- Maintain Payment History: Always pay off your credit before the due date. Even the minimum payment counts, but missing a single payment can negatively impact your score.

- Diversify Your Credit: Relying on just one credit card can hurt your score if you miss a payment. Spread your credit use across multiple accounts to minimize risks.

- Avoid Defaults: Never default on your credit. Defaults significantly damage your score and can take years to recover from.

By focusing on these key factors, you can work towards that perfect 850 credit score.

FICO uses percentages to indicate the significance of each element to your credit scores.

FICO |

|

Factor |

Importance |

| Payment history | 35% |

| Amounts owed | 30% |

| Length of credit history | 15% |

| New credit | 10% |

| Credit mix | 10% |

Importance of a High Credit Score

You may spend less money if you have a high credit score. For instance, customers with excellent credit often get the best deals on loans and credit lines. Over time, you may save paying hundreds of dollars in interest. A good credit score might provide you an advantage when applying for jobs, renting an apartment, or getting a mortgage. A high FICO rating with an 850 fico score might be desired for several reasons, each offering financial savings:

1-Score lower rates on auto loans:

You need more money to purchase a vehicle outright. A good credit score can help you secure a loan with the best terms. Customers with the most noteworthy credit scores meet all requirements for an average loan cost of 4.2% on another car, contrasted with 14.97% for individuals with the least FICO ratings, as Experian information indicates.

2-Get credit cards with great rewards:

You can fit the bill for a credit card with any sort of credit. Yet, the best credit cards regarding prizes and advantages commonly expect great to outsYou’ll probably need an automobile advance unless you have credit scores.

3-Qualify for the lowest rate on a mortgage:

Given the measure of cash included, your home loan is the credit you’ll need to get the minor financing cost conceivable. It merits placing in the additional work to search around and arrange, as even a little rate increment can cost you a considerable number of dollars over the life of your mortgage. Preparing your credit for a home loan is a fundamental advance in the home-buying cycle.

4-Negotiate lower interest rates on your credit cards:

If you are careful of your credit card balance every month, your credit APR is insignificant. But having a great credit score could help you negotiate with your lender to lower your interest rate if you carry a balance. Getting a lower interest rate could spare you a great deal of cash.

5-Improved insurance rates:

If you’re looking for mortgage holders or accident coverage rates, having an excellent FICO rating may assist you with fitting the bill for a lower month-to-month premium- except in certain states where the practice is banned.

6-Refinance your loans to save money:

If you’ve improved your FICO rating since you opened one of your credit accounts, you might have the option to renegotiate it at a lower rate and save cash.

7- Low-interest rate

People with good credit scores often receive the lowest interest rates from lenders when applying for personal, home, or vehicle loans. Throughout a loan, this can result in significant interest cost savings.

8- Unique benefits

Borrowers might receive special benefits from lenders with high minimum credit score criteria.

9-Lender’s possibilities are expanded

You could find it simpler to get approved for credit if you have a perfect or even outstanding credit score. It might give you additional alternatives when comparing lenders, enabling you to be more selective when deciding.

10- Credit card promotions

You may be eligible for discounts like 0% introductory annual percentages rate (APR) credit cards with a high credit score. These credit cards include an initial interest-free for up to 21 months.

11- Become a registered user

If you have a little credit history, ask a family member with great credit to enroll you as an authorized user on one of their oldest credit cards. If the credit card company informs the credit bureaus about authorized users, your credit bureaus about authorized users, your credit score may rise. The drawback is that if the principal cardholder misses a payment and it’s noted on your credit record, your credit score may suffer.

12- Never skimp on payments

You should pay all your payments on time because your payment history makes up 35% of your credit score. Your creditors may send a report to one of the three main credit bureaus, Experian, Equifax, or Transunion after your payment is 30 days past due. The late payment might lower your credit score and stay on your credit report for up to seven years. Enroll in autopay or utilize bill management software to get reminders and monitor all your due dates simultaneously to reduce your chances of missing a payment.

What Factors Determine Your High Credit Score?

Some essential variables determine your credit score. Here are some of the most significant:

- Payment History: Your payment history is one of the most critical elements affecting your credit score. Lenders demand proof that your payments have always been on time; a history of missing or late payments can substantially negatively influence your credit score.

- Credit Utilization: Another crucial aspect is your credit usage ratio, or how much debt you have about your credit limit. Lenders may be reluctant to provide additional credit if they notice that you have a high credit utilization ratio, which might indicate that you’re having trouble managing your debt.

- Credit History: Your credit history’s length is significant because it might give lenders more insight into repayment habits.

- Types of Credit: Your mix of credit accounts, including installment loans, revolving lines of credit, etc.

What Makes up Your Credit Score?

Various factors go into determining your credit score. Some of the most critical factors include:-

- Payment history,

- Credit utilization,

- Credit mix,

- Length of credit history,

- New credit inquiries

- Payment history

Is among the essential elements in determining your score. It is because it shows lenders how you have handled credit. Your credit score will improve if you have a history of on-time payments. Conversely, your score will only improve if you have an account story of missing or making late payments. Another crucial aspect of your score is how much credit you are using. It represents the portion of your credit that is presently being used. Your credit utilization would be 50%; for instance, if you had a credit card, use below 30%; the lower, the better. Your credit mix is taken into account while calculating your score.

What to do if you have a Bad Credit Score?

A subprime loan is given to people, especially borrowers with low credit. Many mortgage lenders only accept people with high credit ratings because of their potential inability to repay the loan. It is also why the interest rate is relatively higher for such loans.

There is a prime interest rate set for premium buyers with a good credit rating; currently, the prime interest rate is 3.25%, but the subprime interest rate is always higher. It is due to the hazard of the low-credit borrower defaulting on the loan altogether.

Even if you’re not a high-risk borrower at your fault, there are chances that you default on the subprime home equity loan because of higher interest rates. Here’s how to avoid getting to that default stage:

- Budget your income to include the potential loan payment.

- Check your score and fix errors in your credit history.

- Make timely payments each month to improve your credit rating.

- Shop around for alternative lenders.

- Consider asking someone with solid credit and income to cosign on loan.

- Set a reminder at least 3-4 days before the due date so that you don’t forget to pay, and if you’re short of money, you have time to ask your friends or family.

What is the average credit score in America in 2022?

The average FICO score in the United States is 716, a new record high and five points higher than 2020. Since 2009, there has been a noticeable uptick in the average U.S. FICO Score, which has grown by 30 points. Nearly 63% of Americans in 2021 had a FICO Score of at least 699. FICO rates a credit score of 716 as “good.” Compared to 2020, the average U.S. VantageScore is 10 Points higher at 698, a new record high.

Can credit scores go above 850?

Yes, credit scores can go above 850. The highest possible credit score is 900. However, scores above 850 are scarce, and most lenders will consider a score of 850 excellent.

Can you raise your credit score by 200 points in a year?

While making some progress in a year is possible, raising your score by 200 points in that timeframe would be tough. A 100-point improvement over a year would be a more attainable objective. Paying your bills on time, keeping your credit card offsets low, and opening various credit accounts are possible.

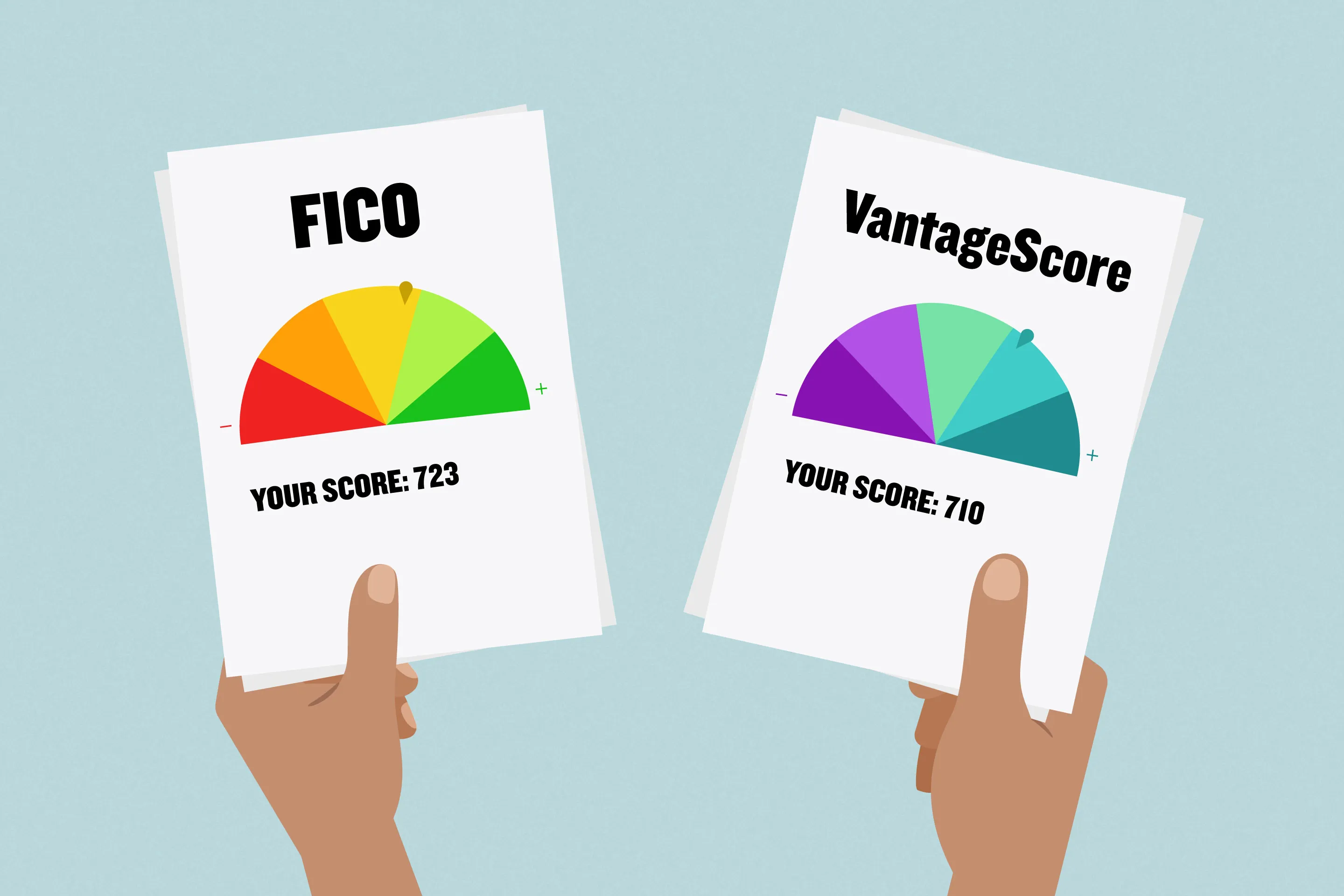

What is a Vantage Score?

An alternative to the FICO credit score is the Vantage Score. Lenders and landlords both utilize it. A Vantage Score is a credit score that the three leading credit agencies jointly established to determine your likelihood of repaying loans. Lenders, landlords, and financial organizations use it to assess creditworthiness.

To compete with the more well-known FICO ratings, credit bureaus Experian, TransUnion, and Equifax developed the algorithm that produces Vantage Score in 2006. Vantage Scores’ most recent modification has a 300 to 850 scale, the same range as FICO’s, but the original scale differed. Vantage Score is readily available to customers for free and has started to catch the eye of lenders.

What’s most important to Vantage Scores?

The VantageScore formula greatly favors the criteria that matter most in FICO scores. Paying on time is the most crucial thing customers can do in both cases to improve their scores. According to VantageScore, credit variables are best described in terms of how “influential” they are to customers’ credit ratings. Its VantageScore 3.0 model dissects the factors:

- The past of payment is “extremely influential.”

- Age and the kind of credit accounts are “highly influential,” as is credit (the proportion of credit limits used).

- Debt and total balances are “moderately influential.”

- The quantity of debt and recent credit behavior is “less influential.”

- However, like FICO, Vantage Score has also defined its rating methodology in percentages.

- 40% of the data includes payment history, which gives it the “extremely influential”

- 20% of the element is credit utilization, combined with the remaining 3% of available credit and the 11% of balances as the general “amounts owed” They have a combined 34% share, which is quite powerful.

- The “depth of credit,” also known as credit age and mix, accounts for 21%.

- 5% of all credit applications are recent.

What Is a Good VantageScore?

The ranges of the first two VantageScore credit rating models were 501 and 990. The 300 to 850 degree is used by the two most recent Vantage Score credit scores (3.0 and 4.0), just as the underlying FICO Scores. Vantage Score classifies 661 to 780 as its excellent range for the most recent models.

VantageScore vs. FICO

The two most popular credit scoring models, FICO and Vantagescore, list 850 as the maximum possible score out of a starting range of 300 to 850.

FICO

Since its launch in 1989, 90% of the top U.S lenders have utilized FICO as their primary evaluation metric. With this model, you may obtain a credit score as high as 850. FICO offers industry-specific ratings designed for credit card firms (FICO Auto score).

Each sector-specific FICO Score, ranging from 250 to 900, emphasizes your financial habits with a particular financial product. Equifax, Experian, and TransUnion are the three major credit reporting bureaus, and each has its version of ratings developed by FICO.

Credit ranking |

Credit mark ranges |

| Exceptional | 800-850 |

| Very good | 740-799 |

| Good | 670-739 |

| Fair | 580-669 |

| Poor | 579-300 |

Vantage Score

Another credit-scoring system that lenders use to assess your creditworthiness is Vantage Score. Equifax, Experian, and TransUnion, the three credit bureaus, worked together to design it. Even though it’s not as popular as FICO, monitoring your Vantage Score is crucial because more than 2,600 financial institutions utilize it. The VantageScore 3.0 and 4.0 models range from 300 to 850, much like FICO. Vantage Score allows you to reach a maximum credit score of 850.

Credit ranking |

Credit mark ranges |

| Excellent | 781-850 |

| Good | 661-780 |

| Fair | 601-660 |

| Poor | 500-600 |

| Very poor | 300-499 |

Tips for Achieving a Perfect Credit Score

There’s no surefire way to achieve a perfect credit score, but there are several things you can do to improve your chances. Make sure expenditures are always made on time first. It is the most essential aspect that will affect your score. Keep your credit card usage minimal and keep a variety of credit accounts. Finally, monitor your credit report often and challenge any mistakes. Paying attention to these proposals may increase your opportunity of getting a perfect credit score. Your credit score influencing factors: payment history, credit utilization, length of credit history, and a variety of credit kinds are just a few of the variables that go into calculating your score. By concentrating on these critical areas, you can raise your score. Your payment past is one of the most essential components of your credit score.

Follow these five measures to increase your chance of getting a perfect credit score. Although there is no assurance that you will succeed in achieving perfection, you could raise your score.

Never skimp on payments

You should pay all your payments on time because your payment history makes up 35% of your credit score. Your creditors may send a report to one of the three main credit bureaus, Experian, Equifax, or Transunion after your payment is 30 days past due. The late payment might lower your credit score, stay on your credit score, and remain on your credit report for up to seven years.

Enroll in autopay or utilize bill management software to get reminders and monitor all your due dates simultaneously to reduce your chances of missing a payment.

Maintain a low credit utilization rate

Your credit utilization ratio, up to 30% of your credit score, is the second most significant element. Your credit utilization ratio calculates how much credit you are currently using compared to how much you have available. A balance closer to 0% will assist in raising your credit score even more; however, it’s often advised to keep it around 30%.

Avoid requesting credit too frequently

Lenders pull your credit when you ask for a loan, which is a complex credit query on your report. Your report will reflect this investigation for up to two years. Each new hard credit inquiry might reduce your score by up to five points, according to FICO. It could prevent you from getting a perfect credit score, even if the effects of this kind of credit check fade with time.

Check your credit report

Errors do occur in credit reports. Your credit score may suffer if a creditor provides the credit bureaus with incomplete or erroneous negative information. Reviewing your credit reports at least once a year will help you find and correct reporting problems. Visit AnnualCreditReport.com to check all three of your credit reports for free. There is typically just one free viewing each year. However, you may still get free weekly reports until December 31, 2022, because of the Covid-19 epidemic.

Become a registered user

Ask a family member with great credit to enroll you as an authorized user on one of their oldest credit cards. Your credit score may rise if the credit card company informs the credit bureaus about authorized users. The drawback is that if the principal cardholder misses a payment and it’s noted on your credit record, your credit score may suffer.

FAQs

Impact does a credit score of 850 have?

Any new loans or credit cards you apply for are more likely to be accepted if your credit score is 850 or higher. Additionally, you’ll probably be qualified for the best interest rates. These are just a few advantages of having a high score.

What are the most common credit scores?

Vantage Score and your FICO Score are two of the most well-known business and credit ratings. Nevertheless, there are many businesses with unique credit ratings and processes. You have various credit ratings as a result.

Banks use what credit score?

Depending on their geographic location and other considerations, multiple banks, lenders, and credit card firms may utilize different credit ratings. Experian, Equifax, and TransUnion are the three most well-known credit bureaus used by various credit score companies. Suppose you’re unsure of the companies. If you’re unsure of the score your bank employs, you might be able to find out by contacting customer service or by searching online.

Conclusion

A high credit score unlocks numerous advantages, including low-interest loans and better rates on credit-driven expenses like insurance premiums. You’ll also benefit from a lower credit utilization rate. Individuals with top scores often use less than 7% of their available credit. Even small steps to improve your score can lead to significant rewards, allowing you to enjoy these perks with minimal effort. By prioritizing your credit health, you open doors to financial opportunities and long-term savings.

{kind=link}

{kind=link}

:max_bytes(150000):strip_icc()/highest-credit-score-it-possible-get-it.asp_final-e168896f17fd404ab990455ca7a83365.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}